Understanding Critical Illness Life Insurance for Seniors

The term a specialized insurance policy that provides a lump sum benefit when you’re diagnosed with a serious medical condition like cancer, heart attack, or stroke. This financial protection helps cover medical expenses, daily living costs, and other bills that Medicare doesn’t fully pay.

If you’re wondering “what is critical illness insurance and do I need it as a senior,” here’s the simple answer: Unlike traditional health insurance, critical illness life insurance for seniors gives you cash directly. You decide how to use it, whether for experimental treatments, home modifications, or simply keeping up with household expenses while you recover.

For Americans over 65, critical illness life insurance for seniors offers peace of mind when health challenges arise. Many people ask “how does critical illness insurance work for older adults” or “should I get critical illness coverage after retirement.” This comprehensive guide explains everything you need to know about securing this vital coverage.

Table of Contents

[Compare Quotes Now to Lock In Lower Premiums]

Why Seniors Need Critical Illness Coverage

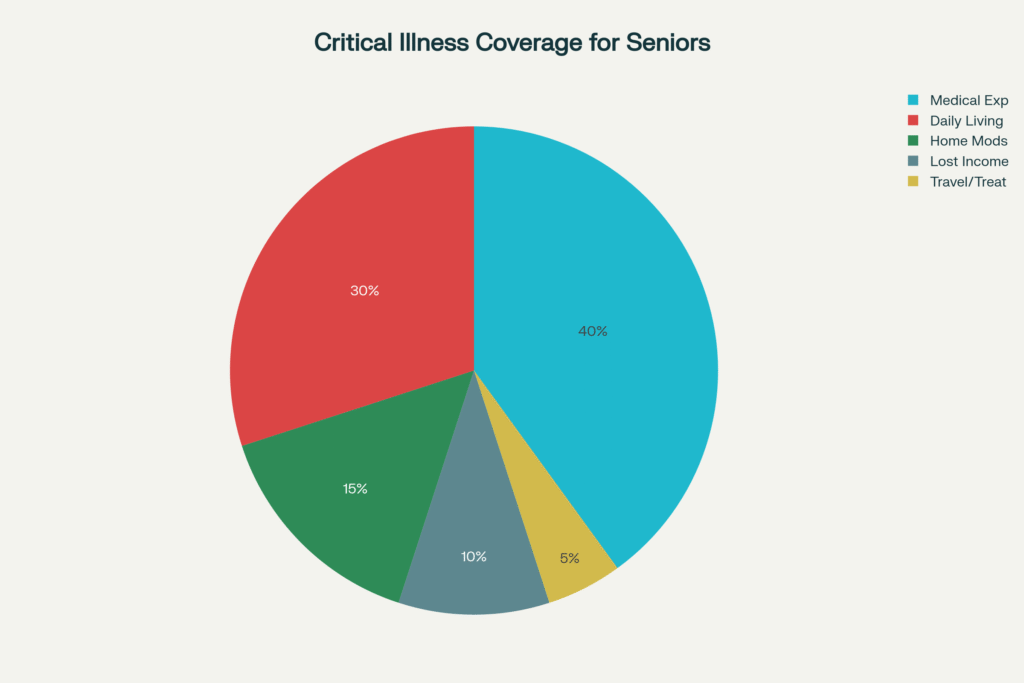

Many seniors wonder “does Medicare pay for everything when I get sick” or “what medical costs aren’t covered by Medicare.” The truth is Medicare covers many medical services, but it doesn’t cover everything. Critical illness life insurance for seniors fills important gaps.

If you’re asking yourself “what happens if I can’t afford my medical bills on a fixed income,” critical illness coverage can help.

What Medicare Doesn’t Cover:

- Deductibles and copayments that add up quickly

- Experimental or out-of-network treatments

- Home healthcare beyond limited periods

- Lost income if you’re still working part-time

- Travel costs for specialized treatment

- Household help during recovery

“After my husband’s stroke, we received $25,000 within two weeks. That money paid for a wheelchair ramp, in-home care, and gave us breathing room when I couldn’t work. Medicare covered the hospital, but not our life.” –Patricia R., Age 68, Florida

[Download Your Free Coverage Assessment Checklist]

How Critical Illness Insurance Works for Retirees

Many retirees ask “how do I actually get money from critical illness insurance” or “what’s the process for filing a claim.” The process is straightforward and designed with seniors in mind.

Step 1: Choose Your Coverage

Select a benefit amount between $10,000 and $50,000 or more. Higher amounts mean higher premiums.

Step 2: Apply

Most policies require basic health questions. Some offer guaranteed issue options with no medical exam.

Step 3: Pay Monthly Premiums

Premiums stay level in many policies, though some increase with age brackets.

Step 4: Receive Your Benefit

Upon diagnosis of a covered illness, file a claim. Most insurers pay within 14 to 30 days.

Step 5: Use Funds As Needed

The lump sum benefit is yours to use without restrictions.

[Use This Benefit Calculator to Estimate Your Coverage Needs]

Covered Illnesses and Conditions

If you’re asking “what diseases are covered by critical illness insurance” or “will my insurance pay if I have a heart attack,” here’s what you need to know. Critical illness life insurance for seniors typically covers these major health events:

Primary Covered Conditions

- Heart attack (myocardial infarction)

- Stroke (cerebrovascular accident)

- Cancer (major invasive types)

- Kidney failure requiring dialysis

- Organ transplants (heart, liver, kidney, lung)

- Coronary artery bypass surgery

- Paralysis from injury or illness

- Blindness (permanent and total)

Additional Coverage Options

Some policies include chronic illness riders that cover:

- Alzheimer’s disease and dementia

- Parkinson’s disease

- Multiple sclerosis

- ALS (Lou Gehrig’s disease)

- End-stage renal disease

“Look for policies that cover the conditions most common in your family history. My mother had breast cancer, so that coverage was essential for me.” Dr. James Martinez, Geriatric Care Specialist

Comparing Top Providers for Seniors

Here’s how major insurers stack up for critical illness life insurance for seniors:

| Provider | Age Limit | Benefit Amounts | Guaranteed Issue | Notable Features |

|---|---|---|---|---|

| Aflac | Up to 75 | $10K to $50K | No | Cancer-specific plans available; fast claims |

| MetLife | Up to 80 | $5K to $50K | Limited options | Flexible benefit periods; wellness benefits |

| UnitedHealthOne | Up to 64 | $10K to $100K | No | AARP partnership; comprehensive coverage |

| Assurity | Up to 70 | $5K to $25K | Yes (age 50 to 70) | Simplified underwriting; chronic illness riders |

| Mutual of Omaha | Up to 75 | $10K to $30K | Yes | No medical exam; acceptance guarantee |

[Compare All Providers Side by Side with Our Interactive Chart]

Understanding Policy Eligibility for Seniors

Many people over 65 ask “am I too old to get critical illness insurance” or “can seniors over 70 still buy this coverage.” Getting approved for critical illness life insurance for seniors depends on several factors.

Age Considerations

Most critical illness insurance policies have age limits:

- Ages 50 to 64: Broadest selection and best rates

- Ages 65 to 70: Good options but higher premiums

- Ages 71 to 80: Limited providers; guaranteed issue common

- Over 80: Very few options; consider alternatives

Health Requirements

Traditional Underwriting:

- Medical history review

- May require exam or blood work

- Better rates for healthy applicants

Simplified Issue:

- Answer basic health questions

- No medical exam required

- Faster approval process

Guaranteed Issue:

- No health questions asked

- Acceptance guaranteed regardless of conditions

- Higher premiums but easier approval

[Request Your Free Quote Today]

Pre-Existing Conditions and Exclusions

One of the most common questions is “can I get critical illness insurance if I already have diabetes” or “what if I’ve had health problems before applying.” Understanding what’s not covered prevents surprises later.

Common Pre-Existing Condition Rules

If you have a condition before buying critical illness life insurance for seniors, most policies:

- Exclude that specific condition for 12 to 24 months

- May permanently exclude certain chronic conditions

- Offer coverage for new diagnoses after the waiting period

Typical Exclusions

Critical illness policies generally don’t cover:

- Self-inflicted injuries

- Conditions from illegal activities

- Non-invasive cancers (skin cancer types)

- Conditions diagnosed within the waiting period (30 to 90 days)

- Pre-existing conditions during the exclusion period

“I have diabetes, and three insurers initially declined me. I found a guaranteed issue policy that worked, though I pay more. It’s worth it for protection against stroke or heart attack, which run in my family.” – Robert T., Age 72, Arizona

Benefit Amounts and Payout Process

People often ask “how much critical illness insurance should I buy” or “how much money will I get if I’m diagnosed with cancer.” Choosing the right benefit amount affects your financial security.

Selecting Your Benefit Amount

Consider these factors:

Current Medical Costs:

- Average heart attack treatment: $20,000 to $50,000 out-of-pocket

- Cancer treatment: $10,000 to $100,000+ depending on type

- Stroke rehabilitation: $15,000 to $45,000 for first year

Your Personal Situation:

- Existing savings and emergency funds

- Other insurance coverage

- Monthly expenses and bills

- Family support availability

Common Benefit Choices:

| Benefit Amount | Best For | Monthly Premium (Age 65)* |

|---|---|---|

| $10,000 | Supplemental coverage | $45 to $75 |

| $25,000 | Moderate protection | $95 to $150 |

| $50,000 | Comprehensive coverage | $180 to $300 |

*Approximate rates for healthy non-smokers

[Calculate Your Ideal Benefit Amount with Our Tool]

How the Payout Process Works

Filing Your Claim:

- Receive diagnosis from licensed physician

- Notify your insurance company immediately

- Submit claim form with medical documentation

- Wait for claims review (typically 5 to 14 days)

- Receive lump sum payment by check or direct deposit

Most seniors receive their benefit within 14 to 30 days of filing a complete claim.

Benefit Reduction After Age 65 or 70

A common concern is “does my coverage decrease as I get older” or “will I get less money if I’m diagnosed at 75.” Many critical illness life insurance for seniors policies reduce benefits as you age. Understanding this helps you plan.

How Reduction Works

Typical Reduction Schedule:

- Ages 50 to 64: 100% of benefit amount

- Ages 65 to 69: 75% of benefit amount

- Ages 70 to 74: 50% of benefit amount

- Ages 75+: 35% of benefit amount

Example:

If you buy a $40,000 policy at age 62:

- You receive full $40,000 if diagnosed before age 65

- $30,000 if diagnosed at age 68

- $20,000 if diagnosed at age 72

Policies Without Reduction

Some insurers offer level benefit policies:

- Premium savings are lower

- Full benefit paid at any age

- Better for long-term planning

- Slightly higher monthly cost

[Speak to a Licensed Specialist About Level Benefit Options ]

Tax Implications of Critical Illness Payouts

Many seniors ask “do I have to pay taxes on critical illness insurance money” or “will the IRS tax my insurance payout.” Good news: most critical illness benefits aren’t taxable.

IRS Treatment of Benefits

According to IRS guidelines:

- Lump sum benefits: Generally tax-free

- Personal policy payments: Not considered taxable income

- Employer-paid premiums: May affect taxation

“Critical illness insurance proceeds are typically received income-tax-free, similar to life insurance death benefits. Consult your tax advisor for your specific situation.” – Sarah Chen, CPA, Elder Financial Planning

When Benefits Might Be Taxable

Benefits could be taxable if:

- Your employer paid the premiums

- You deducted premiums as medical expenses

- Benefits exceed actual medical costs in specific states

Always consult a tax professional for your individual circumstances.

Premium Costs and Savings Strategies

If you’re wondering “how much does critical illness insurance cost per month for seniors” or “what will I pay for this coverage at age 70,” here’s what you need to know. Critical illness life insurance for seniors costs vary based on age, health, and coverage.

Average Premium Ranges

Monthly Premiums by Age (for $25,000 benefit):

| Age Range | Non-Smoker | Smoker | Guaranteed Issue |

|---|---|---|---|

| 50 to 54 | $65 to $95 | $95 to $135 | $110 to $150 |

| 55 to 59 | $85 to $125 | $125 to $175 | $145 to $195 |

| 60 to 64 | $110 to $160 | $165 to $225 | $185 to $250 |

| 65 to 69 | $145 to $210 | $220 to $300 | $245 to $325 |

| 70 to 75 | $195 to $280 | $290 to $400 | $320 to $450 |

[Use ThisCalculator to Estimate Your Costs]

Ways to Save on Premiums

Shop Around:

- Get quotes from at least 3 to 5 providers

- Compare benefit amounts and features

- Ask about senior discounts

Choose Appropriate Coverage:

- Don’t over-insure beyond your needs

- Consider lower benefit amounts

- Review coverage every few years

Improve Your Health:

- Quit smoking for better rates

- Maintain healthy weight

- Control chronic conditions

Bundle Policies:

- Some insurers discount multiple policies

- Add riders instead of separate policies

- Ask about household discounts

For more comprehensive strategies on reducing costs, read our guide on lower life insurance premiums for seniors on a fixed income.

[Compare Quotes Now to Find the Best Rates]

Chronic Illness Riders and Additional Features

Seniors often ask “what extra benefits can I add to my policy” or “should I get a chronic illness rider with my coverage.” Enhanced coverage options provide broader protection.

What Are Chronic Illness Riders?

These additions cover conditions that aren’t immediately life-threatening but significantly impact daily living.

Common Chronic Illness Coverage:

- Activities of Daily Living (ADL) Limitations: Can’t perform 2+ ADLs (bathing, dressing, eating)

- Cognitive Impairment: Alzheimer’s, dementia diagnosis

- Permanent Disabilities: Long-term care needs

Other Valuable Policy Features

Return of Premium Rider:

- Get premiums back if you don’t file a claim

- Usually after 20 or 30 years

- Higher monthly cost but guarantees return

Recurrence Benefit:

- Additional payment if illness returns

- Common with cancer policies

- Usually after survival period (1 to 5 years)

Wellness Benefits:

- Annual payment for preventive care

- Rewards healthy behaviors

- Typically $50 to $100 per year

Waiver of Premium:

- Stop paying premiums after diagnosis

- Coverage continues without payment

- Valuable for fixed incomes

“I added the chronic illness rider to my policy. Five years later, my father developed Alzheimer’s. Seeing what my mother went through, I’m grateful I have that protection.” – Linda M., Age 66, Ohio

To learn more about enhancing your coverage, explore our detailed guides on life insurance riders for seniors and chronic illness riders for seniors.

Critical Illness vs. Final Expense Insurance

Many people wonder “what’s the difference between critical illness and burial insurance” or “should I buy critical illness or final expense coverage.” Understanding the differences helps you choose wisely.

Key Differences

| Feature | Critical Illness Insurance | Final Expense Insurance |

|---|---|---|

| Purpose | Living expenses during illness | Funeral and burial costs |

| Trigger | Diagnosis of covered illness | Death |

| Benefit Amount | $10,000 to $100,000+ | $5,000 to $25,000 |

| Payout Timing | Upon diagnosis (while alive) | After death |

| Use of Funds | Unrestricted | Typically for final expenses |

| Age Limits | Usually up to 75 or 80 | Up to 85+ |

Which One Do You Need?

Choose Critical Illness Life Insurance for Seniors If:

- You want protection against major illnesses

- Medical bills worry you more than funeral costs

- You’re still working or semi-retired

- You have dependents relying on your income

- You want flexible use of benefits

Choose Final Expense Insurance If:

- You want to cover funeral and burial costs

- You don’t want to burden family with expenses

- You’re over 75 with limited other options

- You have chronic conditions that disqualify you from critical illness coverage

Consider Both If:

- You can afford both premiums

- You want comprehensive protection

- You have family history of serious illness

- You want complete peace of mind

Many seniors find value in having both types of coverage for different needs.

[Compare Both Coverage Types with Our Interactive Tool]

The Application Process Step by Step

If you’re thinking “how hard is it to apply for critical illness insurance” or “what do I need to apply for coverage as a senior,” don’t worry. Applying for critical illness life insurance for seniors is easier than you might think.

Before You Apply

Gather Important Information:

- Current medications and dosages

- Names and addresses of doctors

- Medical history for past 5 to 10 years

- Height, weight, and basic health stats

- Social Security number

- Banking information for payments

Review Your Budget:

- Calculate comfortable monthly premium

- Consider long-term affordability

- Factor in potential increases

Application Steps

Step 1: Get Multiple Quotes

Contact 3 to 5 insurance providers. Compare:

- Monthly premiums

- Benefit amounts

- Covered conditions

- Age limits

- Exclusions

- Additional features

Step 2: Complete the Application

Most applications take 15 to 30 minutes. You’ll answer questions about:

- Personal information (name, address, date of birth)

- Current health status

- Medical history

- Medications

- Lifestyle habits (smoking, drinking)

- Family medical history

Step 3: Medical Underwriting (If Required)

Depending on the policy:

- Guaranteed issue: No medical review needed

- Simplified issue: Phone interview or written questions

- Full underwriting: May require physical exam, blood work, or records review

Step 4: Wait for Approval

Approval times vary:

- Guaranteed issue: Immediate to 48 hours

- Simplified issue: 3 to 7 days

- Full underwriting: 2 to 4 weeks

Step 5: Review and Sign Policy

Read everything carefully. Check:

- Benefit amount is correct

- Premium matches quote

- Covered conditions list

- Exclusions and limitations

- Waiting periods

Step 6: Set Up Payment

Most insurers offer:

- Automatic bank withdrawal

- Credit card payment

- Monthly billing

Your coverage typically begins after the first premium payment and any waiting period (usually 30 to 90 days).

Critical Illness Insurance for Seniors with Chronic Illness

One of the biggest concerns seniors have is “can I still get insurance if I have health problems” or “will they deny me because of my diabetes.” Having existing health conditions doesn’t mean you can’t get critical illness life insurance for seniors.

Common Chronic Conditions

Many seniors have conditions like:

- Type 2 diabetes

- High blood pressure

- High cholesterol

- Arthritis

- COPD or asthma

- Previous heart issues

Finding Coverage Options

Best Strategies:

Try Standard Policies First:

Some insurers are more lenient than others. You might qualify for regular rates.

Look for Condition-Specific Plans:

- Diabetic-friendly policies

- Cardiac history acceptance programs

- COPD-specialized coverage

Consider Guaranteed Issue:

No health questions asked. You will pay higher premiums, but acceptance is certain.

Ask About Graded Benefits:

Some policies offer:

- Reduced benefits in early years

- Full benefits after 2 to 3 years

- Lower premiums than guaranteed issue

“I was declined by two companies because of my diabetes. My agent found a carrier that specializes in diabetic applicants. My rates were only slightly higher than standard.” – George K., Age 69, Texas

Managing Pre-Existing Conditions

Document Your Health Management:

- Keep medication lists current

- Track doctor visits and test results

- Show you’re following treatment plans

- Maintain healthy lifestyle habits

Work with Specialized Agents:

Some insurance agents focus on high-risk or senior applicants. They know which carriers are most accepting.

Be Honest on Applications:

Never hide health information. It can void your policy when you need it most.

Comparing Critical Illness with Supplemental Health Coverage

Seniors frequently ask “what other insurance do I need besides Medicare” or “is critical illness insurance better than a Medicare supplement.” Understanding your options helps you make informed decisions.

Types of Supplemental Coverage

Medicare Supplement (Medigap):

- Covers Medicare deductibles and copays

- Standardized plans (Plan A through Plan N)

- Monthly premiums vary by plan and location

- Doesn’t provide lump sum cash

Hospital Indemnity Insurance:

- Pays fixed amount per hospital day

- Covers inpatient stays only

- Lower premiums than critical illness

- Limited to hospitalization events

Critical Illness Life Insurance for Seniors:

- Pays lump sum upon diagnosis

- Covers outpatient treatment costs

- Unrestricted use of funds

- Higher premiums but broader protection

Cancer Insurance:

- Covers only cancer diagnoses

- More affordable than full critical illness

- Specific to cancer-related expenses

- Good if family history of cancer

Which Combination Works Best?

Basic Protection:

- Medicare Parts A and B

- Medicare Supplement (Medigap)

- Part D prescription coverage

Enhanced Protection:

- Basic protection above

- Hospital indemnity insurance

- Final expense insurance

Comprehensive Protection:

- Basic protection above

- Critical illness life insurance for seniors

- Long-term care insurance

- Final expense insurance

Most financial advisors recommend at least the basic protection, with additional coverage based on your health history, family history, and financial situation.

Real Stories from Seniors with Critical Illness Coverage

If you’re wondering “does this insurance really help when you get sick” or “is critical illness coverage actually worth the money,” learning from others’ experiences helps you understand the real value.

Margaret’s Story: Heart Attack at 67

“I bought my critical illness life insurance for seniors at 62, mostly because my agent recommended it. I felt healthy and almost cancelled it several times to save money. At 67, I had a massive heart attack while gardening.

The hospital bills topped $85,000. Medicare covered most, but I still owed $12,000. My critical illness policy paid $25,000 within three weeks.

That money covered my out-of-pocket costs, paid for cardiac rehab not covered by Medicare, and gave us three months of breathing room. My husband retired early to care for me, and we didn’t panic about money. Best $120 a month I ever spent.”

Thomas’s Story: Cancer Diagnosis at 71

“When I was diagnosed with stage 3 colon cancer, the medical bills were scary. But what really got us was everything else.

My wife had to take time off work. We drove 90 miles each way for treatment, three times a week. We paid someone to handle yard work and household repairs I always did.

The $35,000 from my critical illness policy kept us afloat. We used it for gas, groceries, household help, and supplemental treatments my oncologist recommended but insurance wouldn’t cover. Without it, we would have drained our retirement savings.”

Beverly’s Story: Stroke at 69

“My stroke happened suddenly. One minute I was fine, the next I couldn’t speak or move my right side.

Rehabilitation took eight months. Medicare covered 100 days in a facility, then limited home health visits. We needed so much more.

The $20,000 benefit paid for:

- Extended physical therapy (3 times per week for 6 months)

- Occupational therapy to relearn daily tasks

- Speech therapy to regain communication

- Home modifications (grab bars, shower seat, ramps)

- Transportation to appointments

I’m walking and talking again. That insurance made recovery possible.”

Frequently Asked Questions About Critical Illness Insurance for Seniors

Can you get critical illness insurance after 70?

Yes, and this is one of the most asked questions from older adults. If you’re thinking “am I too old to buy critical illness insurance at 72” or “can seniors in their mid 70s still get coverage,” the answer is yes, but options are more limited. Several companies offer critical illness life insurance for seniors up to age 75 or 80. Mutual of Omaha and Assurity provide guaranteed issue policies for seniors in their 70s. Premiums are higher, and benefit amounts may be capped at $25,000 or less. Some policies also include benefit reduction schedules that lower payouts after certain ages.

What illnesses are covered by critical illness insurance?

Many people ask “will it pay if I get cancer” or “does it cover heart attacks and strokes.” Most critical illness life insurance for seniors covers major health events including heart attack, stroke, invasive cancer, kidney failure, organ transplants, coronary bypass surgery, paralysis, and blindness. Some policies include additional conditions like Alzheimer’s disease, Parkinson’s, ALS, and major burns. Coverage varies by carrier and policy, so review the specific conditions list before purchasing.

Is critical illness payout taxable in the US?

Generally, no. Critical illness life insurance for seniors benefits are typically received tax-free when you pay the premiums yourself. The IRS treats these payments similarly to life insurance benefits. However, if your employer paid the premiums or you deducted premiums as medical expenses, taxation rules may differ. Consult a tax professional for your specific situation.

What’s the best critical illness insurance for elderly adults?

The best critical illness life insurance for seniors depends on your age, health, and needs. For healthy seniors 65 to 70, Aflac and MetLife offer competitive rates and comprehensive coverage. For those with health issues, Mutual of Omaha and Assurity provide guaranteed issue options. Consider benefit amounts, covered conditions, premium costs, and any benefit reductions when comparing policies.

Does Medicare cover critical illness?

This is a crucial question seniors ask: “if I have Medicare do I still need critical illness insurance” or “doesn’t Medicare pay for everything.” No. Medicare covers medical treatment but doesn’t provide cash payments for critical illness diagnoses. Medicare pays doctors, hospitals, and other providers directly. Critical illness life insurance for seniors gives you a lump sum to use however you need, whether for medical bills, living expenses, or other costs. The two types of coverage work together but serve different purposes.

How do critical illness plans work for retirees?

If you’re asking “what happens after I buy the policy” or “how do I get paid when I get sick,” here’s the process. Retirees pay monthly premiums to maintain critical illness life insurance for seniors. Upon diagnosis of a covered condition, they file a claim with medical documentation. The insurer reviews the claim and typically pays the lump sum benefit within 14 to 30 days. Retirees can use the money for any purpose without restrictions, including medical bills, household expenses, or treatment not covered by Medicare.

What exclusions apply for seniors with critical illness insurance?

Common exclusions include self-inflicted injuries, conditions from illegal activities, non-invasive cancers (like most skin cancers), and pre-existing conditions during the exclusion period (usually 12 to 24 months). Most policies also have a waiting period of 30 to 90 days after purchase before coverage begins. Pre-existing conditions may be permanently excluded or covered after a waiting period.

Can seniors with diabetes get critical illness insurance?

This is a top concern: “they rejected me because of my diabetes, can I still get coverage somewhere” or “where can diabetics get critical illness insurance.” Yes, though it may be more challenging. Some insurers specialize in critical illness life insurance for seniors with chronic conditions like diabetes. Options include simplified issue policies with lenient underwriting, condition-specific plans, or guaranteed issue policies that accept all applicants regardless of health. Premiums will be higher, and some policies may exclude complications from your existing condition.

How does critical illness insurance work with heart disease history?

Seniors with heart disease history can obtain critical illness life insurance for seniors through guaranteed issue or specialized underwriting programs. Some carriers offer policies specifically designed for cardiac patients. Previous heart attacks or bypass surgery may be excluded from coverage, but new conditions or different illnesses would still be covered. Premiums reflect the higher risk profile.

What’s the difference between critical illness and disability insurance for seniors?

Disability insurance replaces income if you can’t work due to illness or injury. Critical illness life insurance for seniors pays a lump sum upon diagnosis of specific conditions, regardless of work status. Most seniors are retired, making disability insurance less relevant. Critical illness coverage addresses medical costs and living expenses that Medicare doesn’t cover fully.

How long does it take to receive your benefit after diagnosis?

People want to know “how fast will I get my money” or “how long before the insurance pays me.” Most insurance companies pay claims within 14 to 30 days after receiving complete documentation for critical illness life insurance for seniors. Some insurers like Aflac advertise claims processing in as little as 4 business days. The timeline depends on how quickly you submit required paperwork, including physician diagnosis, medical records, and the completed claim form.

What happens if you’re diagnosed with multiple covered illnesses?

This varies by critical illness life insurance for seniors policy. Some policies pay the benefit only once, regardless of how many conditions you develop. Others offer multiple payouts for different conditions, either at the same time or over your lifetime. Some policies provide reduced benefits for subsequent diagnoses. Check your specific policy for multi-condition payment terms.

Should seniors buy critical illness insurance if they have Medicare and a supplement?

A common question is “I already have Medicare and a supplement, why would I need more insurance” or “isn’t Medicare enough coverage.” It depends on your financial situation. Medicare and supplements cover medical treatment costs, but critical illness life insurance for seniors provides cash for non-medical expenses like lost income, household help, travel for treatment, and experimental therapies. If a serious illness would strain your finances beyond medical bills, critical illness coverage adds valuable protection.

Can you cancel critical illness insurance for seniors if you no longer need it?

Yes, most critical illness life insurance for seniors policies can be cancelled at any time without penalty. However, if you cancel and later want coverage again, you’ll need to reapply. Your age and health at that time may result in higher premiums or denial of coverage. Some policies offer return of premium riders that refund your premiums if you cancel after a certain period.

Is critical illness insurance worth it for seniors over 75?

Older adults often ask “should I buy this at my age” or “is it too expensive for people over 75.” For seniors over 75, critical illness life insurance for seniors becomes more expensive with fewer options and lower benefit amounts. If you have substantial savings ($50,000+), the value may be limited. However, if you have limited savings, pre-existing conditions, or family history of serious illness, guaranteed issue policies still provide valuable protection despite higher costs.

How does critical illness insurance for seniors with COPD work?

Many with breathing problems wonder “can I get coverage if I have COPD” or “will they insure me with lung disease.” Seniors with COPD can obtain critical illness life insurance for seniors through guaranteed issue policies that don’t require health questions. Some insurers offer simplified issue policies with questions about COPD severity. While COPD complications might be excluded, you’d still receive benefits for heart attack, stroke, cancer, or other covered conditions unrelated to your respiratory condition.

Making Your Decision: Is Critical Illness Life Insurance for Seniors Right for You?

Consider these factors when deciding about critical illness life insurance for seniors.

You May Benefit from Critical Illness Coverage If:

- You have limited savings to cover major medical events

- Family history includes heart disease, cancer, or stroke

- You’re still working part-time and need income protection

- Medicare gap coverage concerns you

- You want financial flexibility during health crises

- You have dependents who rely on your support

You May Not Need Critical Illness Coverage If:

- You have substantial emergency savings ($50,000+)

- You have comprehensive health insurance through work

- You’re in excellent health with no family history of serious illness

- You already have multiple supplemental policies

- Premium costs strain your fixed income

- You’re over 80 with very limited coverage options

Questions to Ask Yourself:

- Could I afford $15,000 to $30,000 in unexpected medical costs?

- What would happen to my household if I couldn’t work for 6 months?

- Do I have family who could financially support me during serious illness?

- Am I at higher risk due to family history or lifestyle?

- Can I comfortably afford the monthly premiums long-term?

Taking the Next Steps

Ready to explore critical illness life insurance for seniors? Here’s what to do.

Step 1: Assess Your Needs

Use the Critical Illness Coverage Assessment Checklist (downloadable at end of article):

- Calculate potential out-of-pocket medical costs

- Review your current insurance coverage

- Identify gaps in protection

- Determine comfortable benefit amount

- Set realistic premium budget

Step 2: Research Providers

Contact multiple insurance companies:

- Request quotes from 3 to 5 carriers

- Compare coverage details side by side

- Read customer reviews and ratings

- Check company financial strength ratings (AM Best, Standard & Poor’s)

- Verify company licenses with your state insurance department

Step 3: Speak with an Insurance Professional

Find an independent agent who:

- Specializes in senior insurance products

- Represents multiple carriers

- Explains options clearly without pressure

- Answers all your questions thoroughly

- Provides written comparison of recommendations

Step 4: Review Before Buying

Before signing any application:

- Read the entire policy document

- Understand all exclusions and limitations

- Verify benefit amounts and premiums

- Confirm waiting periods and reduction schedules

- Ask about free look period (usually 10 to 30 days to cancel)

Step 5: Keep Good Records

After purchasing:

- Store policy documents in a safe place

- Share policy information with family members

- Keep contact information easily accessible

- Review coverage annually

- Update beneficiaries as needed

Summary: Protecting Your Financial Health

Critical illness life insurance for seniors provides crucial financial protection when serious health events occur. This coverage delivers a lump sum benefit upon diagnosis of conditions like heart attack, stroke, or cancer, giving you cash to use as needed during recovery.

Key Takeaways:

- Medicare doesn’t cover all costs associated with critical illness

- Benefits are typically paid within 14 to 30 days of diagnosis

- Most payouts are tax-free for personal policies

- Critical illness life insurance for seniors is available into your 70s and sometimes 80s

- Guaranteed issue options exist for those with pre-existing conditions

- Premiums vary based on age, health, and benefit amount ($10,000 to $50,000+)

- Many policies reduce benefits after age 65 or 70

- Coverage complements but doesn’t replace Medicare or supplements

The decision to purchase critical illness life insurance for seniors depends on your personal financial situation, health history, and peace of mind priorities. For many seniors, the security of having immediate cash available during a health crisis outweighs the cost of monthly premiums.

Take action today to protect your tomorrow.

Download Your Free Critical Illness Coverage Assessment Guide

Get the comprehensive checklist and planning guide to help you:

- Evaluate your current coverage gaps

- Calculate your ideal benefit amount

- Compare provider options systematically

- Prepare for the application process

- Ask the right questions before buying

- Organize policy documents properly

This 12-page PDF includes:

- Coverage Needs Calculator

- Provider Comparison Worksheet

- Application Preparation Checklist

- Important Questions to Ask Agents

- Policy Review Template

- Claims Filing Guide

- Senior-Friendly Tips for Managing Your Policy

Additional Resources

Government and Non-Profit Organizations:

- Medicare.gov – Official Medicare information and coverage details

- AARP – Senior advocacy and insurance guidance

- National Council on Aging – Benefits and assistance programs

- CDC – Health statistics and disease prevention information

Insurance Industry Resources:

- National Association of Insurance Commissioners (NAIC) – Consumer protection and complaint filing

- AM Best – Insurance company financial strength ratings

- Better Business Bureau – Company reputation and complaint records

Tax and Financial Planning:

- IRS.gov – Tax treatment of insurance benefits

- National Association of Personal Financial Advisors – Find certified financial planners

- Financial Planning Association – Financial education resources

Always verify information with qualified professionals before making decisions about critical illness life insurance for seniors.

Disclaimer: This article provides general information about critical illness life insurance for seniors for educational purposes only. It does not constitute financial, legal, or insurance advice. Consult with licensed insurance professionals and financial advisors for guidance specific to your situation. Policy terms, benefits, and availability vary by state and carrier.