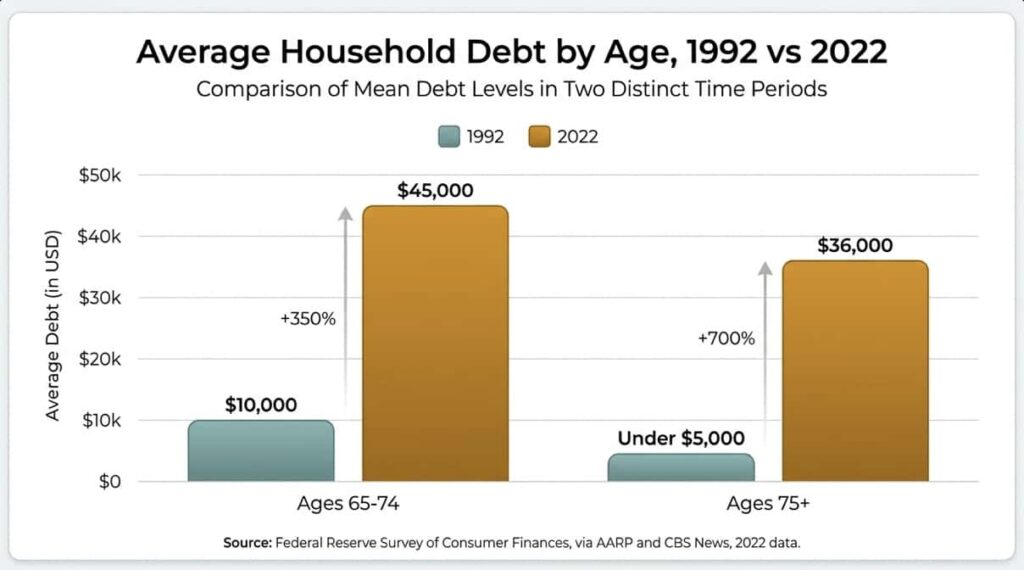

Avoiding debt in retirement has become harder than it was for previous generations, and the numbers prove it. A recent Nationwide study found that Americans of retirement age now carry an average of $70,000 in debt. For households headed by someone aged 65 to 74, average debt has more than quadrupled over the last three decades, climbing from about $10,000 in 1992 to around $45,000 in 2022, according to Federal Reserve Survey of Consumer Finances data reported by CBS News. For those 75 and older, the increase is even steeper – a sevenfold jump from under $5,000 to $36,000 over the same period, per AARP.

This guide focuses on avoiding debt in retirement using verified data rather than fear-based generalizations. You will see exactly which debt types are driving the increase, why credit cards are the most dangerous category on a fixed income, and the specific, actionable steps that reduce risk before and during your retirement years.

Table of Contents

A Note From the Researcher Behind This Guide

I am a personal finance researcher, but I think of myself as a guide through confusing paperwork.

My journey started with a shoebox of insurance documents and countless afternoons at my grandmother’s kitchen table, where she would puzzle over fine print between teaching me her favorite recipes. She was sharp as a tack. But those statements, bills, and minimum-payment notices still baffled her in her later years.

I watched her juggle a fixed income against rising costs and quietly worry about money she had worked her whole life to manage well. Watching her navigate that pressure made it my mission to cut through the confusion for every family like hers. That same promise drives this guide: no jargon, no scare tactics, just verified numbers and practical steps for avoiding debt in retirement – the kind of clarity I first sketched for Grandma on a piece of notepaper at that same kitchen table.

Why Avoiding Debt in Retirement Is Harder Than It Used to Be

Unlike previous generations, which widely entered retirement with modest debt balances or none at all, today’s retirees are carrying more debt, and more kinds of it, according to CBS News reporting on Federal Reserve data. Three forces explain why avoiding debt in retirement has become significantly more difficult.

Debt now follows people deeper into old age. The share of older households carrying any debt rose from 58 percent in 1989 to 71 percent in 2016, according to a GAO analysis of Survey of Consumer Finances data. Household debt among those 75 and older more than doubled to nearly $41,000 on average in the wake of the 2008 financial crisis, and after a sharp decline by 2013, it has been rising steadily since, driven in large part by the inflation spike of 2021 and 2022.

Wages rise with inflation. Fixed incomes do not. While painful for all consumers, higher prices are more easily absorbed by people in the workforce because wages typically rise alongside prices. Retirees living on Social Security, a pension, or fixed savings withdrawals do not have that same buffer. As AARP’s Lori Trawinski explains, this gap is one of the central reasons avoiding debt in retirement now requires more deliberate planning than it once did.

Credit card debt fills the gaps that fixed income cannot cover. Unlike mortgages, auto loans, or student loans, which follow predictable payment schedules, credit card debt is revolving and high interest. It tends to build quietly, particularly for retirees using credit cards to cover everyday essentials like groceries, gas, prescriptions, and utilities when monthly income falls short. About 65 percent of older adults with debt say it is a problem, and nearly a third call it a major problem, according to an October 2023 AARP study.

When my grandmother was managing her finances in her final years, what struck me most was how invisible the slide into revolving debt can be. A few groceries here, a prescription copay there, none of it dramatic in the moment. By the time the statement arrived, the balance had grown in a way that felt sudden but was actually gradual. Avoiding debt in retirement means watching for that slow creep before it becomes a structural problem.

The Debt Types That Make Avoiding Debt in Retirement So Difficult

Not all debt carries the same risk for someone living on a fixed income. Understanding the difference is the foundation of avoiding debt in retirement successfully.

Credit Card Debt: The Biggest Obstacle to Avoiding Debt in Retirement

Credit card debt is one of the biggest problems seniors face today, according to financial professionals interviewed by AARP. The average credit card debt per American was $6,715 as of December 2025, according to TransUnion data reported by Forbes Advisor. The average interest rate on credit card accounts assessed interest was 21.52 percent as of February 2026, per the Federal Reserve.

That interest rate is what makes credit cards uniquely dangerous for avoiding debt in retirement. A balance of $6,715 at 21.52 percent APR, paid down at $150 a month, takes more than 93 billing cycles and costs over $7,000 in interest alone, according to Forbes Advisor calculations. On a fixed income with no way to absorb a sudden income shock, that math compounds quickly.

Experts noted in GAO’s analysis that credit card debt has uniquely negative implications for older Americans’ retirement security because credit cards often carry high, variable interest rates and are not secured by any asset. This is precisely why avoiding debt in retirement starts with treating credit card balances as the top financial priority to eliminate.

Mortgage Debt: Not Automatically a Problem

Carrying housing debt into retirement is not always a negative strategy, according to the National Council on Aging. For homeowners who benefited from low interest rates locked in years ago, mortgage debt can remain manageable within a fixed budget. In 2019, a little more than 1 in 4 older adult households were still paying a mortgage after age 65, per NCOA data.

An increase in mortgage debt may actually have positive effects on retirement security, since a home is generally a wealth-building asset, according to experts cited in the GAO report. The nuance that matters for avoiding debt in retirement is this: a mortgage with a low fixed rate, on a home you intend to keep, is a fundamentally different risk than revolving high-interest consumer debt.

Medical Debt: Rising Even With Insurance

Despite the majority of Americans having health insurance, medical debt continues to rise and poses a significant barrier to economic well-being for older adults, according to NCOA. In 2020, nearly 4 million adults age 65 and older, or 7 percent, had unpaid medical bills. Medicare does not cover everything, leaving retirees responsible for deductibles, copays, dental work, and other costs that frequently end up on credit cards, per CBS News reporting.

Auto Loan Debt: Smaller but Still Present

Auto debt climbed to roughly $1.66 trillion nationally in Q2 2025, and while delinquency rates concentrate most heavily among borrowers under 30, auto loans remain a recurring fixed obligation for many retirees who need reliable transportation, according to Carry’s analysis of Federal Reserve data.

The Trade-Offs Older Adults Are Already Making to Manage Debt

The financial pressure behind avoiding debt in retirement is producing real behavioral changes, and the data on this is sobering. Among aging network professionals surveyed by the National Council on Aging, 23 percent regularly encounter seniors forgoing needed home or car repairs, which increases the risk of falls, the leading cause of injuries among seniors. Nearly 15 percent regularly encounter seniors cutting pills in half to stretch their medication supply, which can limit the medication’s effectiveness.

Separately, a 2025 Clever Real Estate survey of 1,000 American retirees found that roughly 1 in 7 retirees, or 14 percent, have avoided medical appointments or treatments to preserve retirement savings, and 1 in 8, or 12 percent, admit to skipping meals for the same reason. About 29 percent of those surveyed reported having no retirement savings at all.

These figures matter because they show what happens when avoiding debt in retirement fails: the trade-offs do not stop at finances. They extend directly into physical health and safety.

Step-by-Step: A Practical Plan for Avoiding Debt in Retirement

Avoiding debt in retirement is achievable with a structured plan, whether you are years away from retiring or already managing debt on a fixed income today.

Step 1: Identify and Rank Every Debt by Interest Rate

List every debt you carry: credit cards, mortgage, auto loan, medical bills, and any personal loans. Note the interest rate and minimum payment for each. Credit card debt at 21 percent or higher should always be addressed before lower-rate, secured debt like a mortgage at 6 percent. This single step is the most important part of avoiding debt in retirement, because it tells you exactly where your money is doing the most damage.

Step 2: Attack High-Interest Debt Before Anything Else

Consolidating credit card debt into a lower-rate instrument like a personal loan can meaningfully reduce what you spend on interest. Moving a balance from a 22 percent credit card rate down to a 7 to 10 percent personal loan rate is a significant improvement, according to financial advisors cited by AARP. However, advisors caution that consolidation only works if you also address the spending behavior that created the balance in the first place, since people who have grown used to borrowing tend to keep doing so unless the underlying habit changes.

Step 3: Consider Working a Few Additional Years if Debt Is High

If you are nearing retirement with substantial debt, an extra year or two of full-time income can make a measurable difference. According to Nasdaq’s analysis of Nationwide’s $70,000 average debt figure, an additional year or two of earning could enable a retiree to whittle a $70,000 balance down to $30,000 or $40,000, or potentially eliminate it before retiring entirely. This step is not available to everyone, but for those who have the option, it is one of the most effective tools for avoiding debt in retirement.

Step 4: Build a Realistic Budget Around Your Actual Fixed Income

Avoiding debt in retirement requires an honest budget built around Social Security, pension income, and planned withdrawal rates, rather than around pre-retirement spending habits. The National Council on Aging recommends creating a budget calendar to understand exactly where money is going each month, which makes it far easier to catch the early signs of revolving credit use before the balance grows.

Step 5: Treat Medical Costs as a Separate Line Item

Because Medicare does not cover all medical costs, build a specific budget line for deductibles, copays, and dental expenses rather than letting them default onto a credit card. NCOA’s data shows that medical debt is one of the three most common forms of debt carried by older adults, alongside credit cards and mortgages, and planning for it directly is one of the most overlooked steps in avoiding debt in retirement.

Step 6: Use Gig or Part-Time Income to Chip Away at Existing Balances

If you are already retired and carrying debt, the gig economy offers a way to generate extra income specifically earmarked for debt paydown, rather than letting balances linger indefinitely, according to Nasdaq’s retirement debt analysis. Even modest, consistent extra income directed entirely at the highest-interest balance accelerates payoff far faster than minimum payments alone.

Step 7: Get a Free, No-Pressure Look at Your Insurance and Income Gaps

Avoiding debt in retirement is not only about debt itself. It also means making sure unexpected costs, like a medical emergency or a spouse’s final expenses, do not become a brand-new source of high-interest borrowing. Mutual of Omaha’s life insurance calculator provides a free, no-obligation way to see what coverage might cost based on your age and state, helping you understand whether a small monthly policy could prevent a much larger debt event later. AARP’s life insurance comparison tool offers a similar free resource with no personal information required for a baseline estimate.

For related planning resources, see our guides on affordable life insurance options for seniors on a fixed income and lower life insurance premiums for seniors on a fixed income.

Frequently Asked Questions About Avoiding Debt in Retirement

What is the average debt for someone at retirement age?

Americans of retirement age carry an average of $70,000 in debt, according to a Nationwide study reported by Nasdaq. For households aged 65 to 74 specifically, average debt was approximately $45,000 in 2022, up from $10,000 in 1992, according to Federal Reserve data cited by CBS News.

Is mortgage debt as risky as credit card debt for retirees?

No. Experts interviewed by GAO note that mortgage debt, particularly at a low fixed rate, can have positive effects on retirement security since a home is a wealth-building asset. Credit card debt, by contrast, is unsecured and typically carries interest rates above 20 percent, making it far more damaging to a fixed income. Avoiding debt in retirement should prioritize eliminating high-interest unsecured debt first.

Why is credit card debt rising so fast among older adults specifically?

Credit card debt is revolving and tends to build quietly as retirees use it to cover gaps between fixed income and rising costs for groceries, gas, prescriptions, and utilities, according to CBS News. Average credit card interest rates above 21 percent compound this problem significantly faster than for other debt types.

Can working longer actually help with avoiding debt in retirement?

Yes, for those who have the option. An additional year or two of full-time income before retiring can reduce a $70,000 debt balance to $30,000 or $40,000, or eliminate it entirely in some cases, according to Nasdaq’s analysis of Nationwide retirement debt data.

What trade-offs are seniors already making because of retirement debt?

According to the National Council on Aging, 23 percent of aging network professionals surveyed regularly see seniors skip needed home or car repairs, and nearly 15 percent see seniors cutting pills to stretch medication supply. Separately, a 2025 Clever Real Estate survey found that 14 percent of retirees have avoided medical care and 12 percent have skipped meals to preserve savings.

The Bottom Line on Avoiding Debt in Retirement

Avoiding debt in retirement is no longer a given, even for households that planned carefully during their working years. The data is unambiguous: average debt among Americans 65 to 74 has more than quadrupled since 1992, and credit card interest rates above 21 percent make revolving balances especially dangerous on a fixed income.

The good news is that the solution does not require complicated financial engineering. It requires ranking debts by interest rate, attacking the highest-rate balances first, building a budget around actual fixed income rather than old spending habits, and treating medical costs as a planned expense rather than a surprise that lands on a credit card.

At my grandmother’s kitchen table, surrounded by her bills and her bank statements in her later years, I learned that the difference between manageable debt and a financial crisis often came down to catching the slide early and naming it honestly. That is what this guide, and everything on this site, is here to help you do.

Data sources: U.S. Government Accountability Office, “Retirement Security: Debt Increased for Older Americans over Time” (GAO-21-170); Federal Reserve Survey of Consumer Finances, via CBS News (2025) and AARP (2023, 2024); National Council on Aging, “Get the Facts on Senior Debt”; TransUnion credit data via Forbes Advisor (2026); Federal Reserve G.19 Consumer Credit Report (2026); Nationwide Retirement Institute data via Nasdaq; Clever Real Estate 2026 retiree survey (1,000 respondents, October 2025). All figures represent the most recently published data available at time of writing and are subject to revision as new surveys are released. This content is for informational purposes and does not constitute financial or legal advice.