Best life insurance riders for chronic illness protection are optional policy add-ons that allow an insured individual to accelerate a significant portion of their policy’s death benefit while still living if they are diagnosed with a severe, long-term health condition that limits their functional independence.

When I was looking into this complex corner of the insurance world for my own family, I quickly realized how terrifyingly easy it is to focus purely on what happens after you are gone, completely ignoring what happens if you get seriously sick along the way. The thing that trips up most readers I talk to is the outdated assumption that life insurance only provides value once the policyholder passes away. In today’s financial landscape, living benefits have fundamentally rewritten the rulebook.

If you are a family provider, a senior navigating estate preservation, or someone trying to protect hard-earned retirement assets, selecting the right policy add-ons is paramount. This exhaustive guide will break down how to secure the best life insurance riders for chronic illness protection, how they operate behind the scenes, and how to maximize their utility without dismantling your family’s long-term safety net.

Table of Contents

The Evolution of Living Benefits in Modern Insurance

For generations, traditional life insurance operated as a static, death-benefit-only instrument. You dutifully paid your monthly or annual premiums, and your beneficiaries received a tax-free lump sum after your passing. While that structure remains foundational for income replacement and debt clearance, it left a massive, gaping vulnerability in most financial plans: the financial devastation of surviving a prolonged medical crisis.

As medical advancements in 2026 continue to extend lifespans, surviving a major diagnosis – such as a severe stroke, advanced cardiovascular disease, or progressive neurological disorders – is more common than ever. However, surviving a health crisis is incredibly expensive. Modern health insurance often leaves families with massive out-of-pocket gaps, experimental treatment costs, and specialized home care bills that can easily decimate an investment portfolio in a matter of months.

This exact vulnerability is why the best life insurance riders for chronic illness protection have transitioned from luxury policy extras to mandatory components of a resilient financial strategy. By shifting your coverage from a pure death benefit to a flexible asset that covers both mortality risk and morbidity risk, you build a financial firewall that protects your wealth while you are alive and preserves your legacy when you are gone. Finding the best life insurance riders for chronic illness protection means balancing your current monthly budget with your future medical needs.

Decoding the Technical Triggers: The Six Activities of Daily Living

To successfully utilize the best life insurance riders for chronic illness protection, a policyholder must meet strict, federally standardized medical criteria. Insurance carriers do not pay out these living benefits based on a subjective feeling of illness or generalized fatigue. Instead, the legal framework requires a licensed healthcare practitioner to certify that the insured is unable to perform a specific number of essential physical tasks.

The universal benchmark for triggering a chronic illness acceleration involves the six Activities of Daily Living – commonly referred to as ADLs. To qualify for a benefit payout under a contract offering the best life insurance riders for chronic illness protection, a doctor must document that you cannot independently perform at least two of these six standard activities for a projected period of at least 90 days.

Understanding these six distinct baseline definitions is vital for avoiding surprises when a claim is filed:

- Bathing: The physical capacity to wash oneself thoroughly in a traditional tub, a standard shower, or via a comprehensive sponge bath, including the independent movement of getting into and out of the shower area safely.

- Continence: The complete physiological ability to maintain control over bowel and bladder functions, or the capacity to independently manage all necessary personal hygiene related to an ostomy pouch or a urinary catheter.

- Dressing: The cognitive and physical capability to put on and take off all essential clothing items, including complicated fasteners, medical braces, or necessary artificial limbs without external human assistance.

- Eating: The fundamental mechanical action of feeding oneself by getting nourishment into the body, whether through traditional utensils from a plate or through the direct management of an intravenous or feeding tube setup.

- Toileting: The multi-step physical process of getting to and from the toilet, transferring onto and off the commode, and performing all associated personal hygiene tasks independently.

- Transferring: The baseline mobility required to move one’s body safely into or out of a standard bed, a traditional living room chair, or a specialized wheelchair without relying on another person’s physical support.

Alternatively, if an individual can still perform all six of these physical ADLs but suffers from a severe cognitive impairment – such as advanced Alzheimer’s disease, clinical dementia, or irreversible brain trauma – that requires substantial, constant supervision to protect them from threats to their health and safety, the best life insurance riders for chronic illness protection will still trigger a full payout.

Chronic Illness Riders vs. Long-Term Care Riders: The Definitive Showdown

One of the most persistent hurdles for personal finance researchers is confusing a chronic illness rider with a dedicated long-term care – or LTC – rider. While they sound practically identical on the surface and share similar medical triggers, their structural, legal, and financial frameworks are completely distinct. Misunderstanding these differences can lead to devastating gaps in your coverage when you need it most. Many families spend thousands on separate policies before realizing that the best life insurance riders for chronic illness protection could have solved their core financial concerns in a single contract.

Critical Industry Warning: Never assume a chronic illness rider is identical to a qualified long-term care rider. While both allow you to access living benefits based on ADL deficits, a chronic illness rider often requires your condition to be certified as permanent, whereas an LTC rider can trigger for temporary conditions from which you are fully expected to recover.

To help you visualize these differences and make an informed decision for your estate, let’s map out how these two distinct mechanisms compare across critical policy parameters:

| Policy Metric & Framework | Chronic Illness Rider | Long-Term Care (LTC) Rider |

| Primary Medical Qualification | Inability to perform 2 of 6 ADLs or severe cognitive impairment. | Inability to perform 2 of 6 ADLs or severe cognitive impairment. |

| Expectation of Permanency | Typically requires a doctor to certify the condition is permanent or lifelong. | Does not require permanency; can cover temporary rehab after an illness. |

| Standard Payout Model | Usually follows an indemnity model (direct unrestricted cash). | Frequently follows a reimbursement model (reimburses actual bills). |

| Upfront Premium Impact | Often built into the policy for free or a nominal fee at issuance. | Always requires an additional, explicit premium payment from day one. |

| Use of Benefit Funds | 100% unrestricted; pay for anything from medical bills to a family vacation. | Restricted solely to qualifying medical care, nursing homes, or home aides. |

| Tax Code Governance | Governed strictly under Internal Revenue Code Section 101(g). | Governed primarily under Internal Revenue Code Section 7702B. |

Choosing between these options depends heavily on your budget and your broader financial layout. If you want a low-cost safety net that provides unrestricted cash if you face a catastrophic, permanent health decline, the best life insurance riders for chronic illness protection are an exceptional, budget-friendly solution. If you want comprehensive protection that steps in for temporary medical rehabilitations, a dedicated LTC rider or a standalone policy may be more appropriate. Ultimately, adding the best life insurance riders for chronic illness protection helps ensure your capital stays intact.

The Financial Mechanics: How a Living Benefit Payout is Calculated

When you decide to execute a claim under the best life insurance riders for chronic illness protection, the insurance company does not simply hand over a giant stack of cash without adjusting your policy’s underlying values. The specific method your carrier uses to calculate your payout will heavily dictate how much money you receive in real time and how much legacy is left behind for your family.

Across the modern insurance landscape, companies rely on two primary internal calculation mechanisms: the Lien Method and the Discounted Death Benefit Method. Understanding these financial options will help you select the best life insurance riders for chronic illness protection from top-tier carriers.

The Lien Method

Under the lien method, the insurance company treats your living benefit payout as an advance loan against your own future death benefit. When you request cash via the best life insurance riders for chronic illness protection, the carrier cuts you a check for that exact amount, but they place a formal financial lien against the policy’s face value. They will charge a contractually stated interest rate on that lien balance over time.

The major benefit of this system is that your ongoing premium payments usually remain completely unchanged, and you know exactly how much cash you are extracting from the policy at that moment. The downside, however, is that as interest accumulates on the lien over the years, the remaining death benefit that will eventually be paid out to your heirs shrinks considerably. If you survive for many years after the initial acceleration, the interest drag can severely erode the final legacy you intended to leave behind.

The Discounted Death Benefit Method

This approach is highly common among insurance policies that include living benefits for “free” or at a very low upfront cost during the initial underwriting phase. Under the discounted death benefit method, when you file a claim under the best life insurance riders for chronic illness protection, the insurance company evaluates several moving variables: your current age, the severity of your medical diagnosis, your remaining statistical life expectancy, and current macroeconomic interest rates.

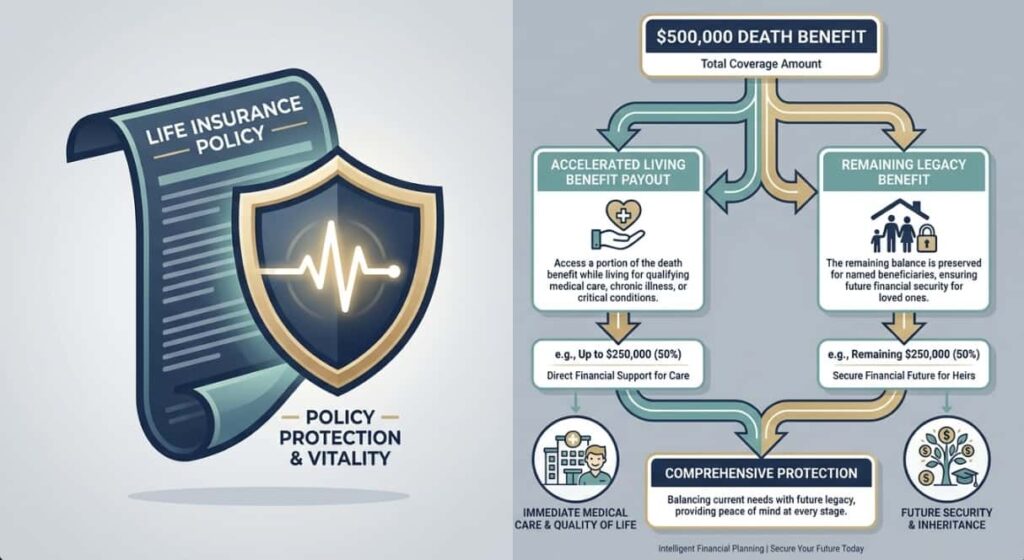

Based on these factors, the insurer will offer you a “discounted” lump sum that is smaller than the actual amount of death benefit you are choosing to surrender. For example, if you request to accelerate $200,000 of your total coverage through the best life insurance riders for chronic illness protection, the insurance company might calculate your specific risk profile and offer you a direct cash payment of $140,000.

If you accept that offer, the full $200,000 is immediately wiped off your policy’s face value, and your remaining death benefit is adjusted downward accordingly. The primary advantage here is that you do not have to worry about a growing interest lien over time – the transaction is entirely clean and finalized the moment the check clears. This clean break is why many buyers prefer the discounted method when adding the best life insurance riders for chronic illness protection to their policy setup.

Navigating the Tax Implications of Internal Revenue Code Section 101(g)

For any personal finance researcher focused on protecting substantial assets, tax compliance is an absolute non-negotiable priority. The tax treatment of living benefits is one of the most attractive features of the best life insurance riders for chronic illness protection, but you must stay strictly within the boundaries of federal guidelines to avoid an unexpected income tax bill.

Under Internal Revenue Code Section 101(g), payouts received from a qualified accelerated death benefit rider are generally treated as life insurance death benefits, meaning they are received entirely free of federal income tax. To qualify for this tax-exempt status, the insured individual must be certified by a licensed medical practitioner as being “chronically ill,” following the exact ADL or cognitive triggers we detailed earlier. Secure contracts containing the best life insurance riders for chronic illness protection to maintain this tax benefit. For more details on alternative structures, you can read my specialized breakdown of accelerated death benefits.

HNW individuals often run into issues because the IRS imposes strict daily limits on tax-free per diem payouts for chronic illness benefits. If your policy operates on an indemnity model – meaning the carrier pays you a flat monthly check regardless of your actual medical bills – any amount you receive that exceeds the annual IRS per diem limit can be classified as taxable income, unless that excess money was used entirely to cover actual, documented out-of-pocket costs for qualified long-term care services.

In 2026, the maximum tax-free per diem limit stands at $430 per day. Because tax codes are inherently fluid and subject to change, it is always an excellent idea to coordinate closely with a certified public accountant or an estate planning attorney before initiating a large-scale acceleration claim under the best life insurance riders for chronic illness protection.

Premium Costs and Underwriting Factors in 2026

When evaluating the best life insurance riders for chronic illness protection, understanding how these add-ons impact your monthly or annual premium is essential for accurate budgeting. The cost structure of these riders typically falls into two distinct categories depending on the type of life insurance policy you select and the specific insurance carrier you partner with. For a broader overview of custom configurations, check out my guide on life insurance riders for seniors.

Upfront Premium Riders

Some carriers require you to pay an explicit, calculated fee from day one to attach a chronic illness rider to your policy. This fee is added directly to your base premium and must be paid continuously over the life of the contract. The benefit of paying this upfront cost is that the carrier typically guarantees a highly favorable, predictable payout formula if you ever need to execute the best life insurance riders for chronic illness protection down the line.

No-Upfront-Cost Riders

Many modern universal life and whole life insurance policies now include the best life insurance riders for chronic illness protection automatically at the time of approval without charging an extra cent on your recurring premium bill. Instead of charging you upfront, the insurance company defers their cost entirely. They apply their fees and financial adjustments only if and when you choose to exercise the rider in the future, using the discounted death benefit method we analyzed previously. You can learn more about how this impacts overall pricing structures in my detailed report on the cost of life insurance with living benefits for senior citizens.

Regardless of the premium structure, securing these living benefits requires passing medical underwriting. Because a chronic illness rider obligates the insurance carrier to potentially pay out hundreds of thousands of dollars years ahead of schedule, underwriters will carefully examine your medical history, current prescription medications, height-to-weight ratio, and family history of hereditary diseases. If you are specifically dealing with severe diagnoses, feel free to read my articles on whole life insurance for seniors with pre-existing conditions or chronic illness riders for seniors.

If you have already been diagnosed with a progressive, degenerative medical condition, you may be declined for the rider or face significantly higher base insurance rates. This reality underscores the absolute importance of securing coverage as early as possible while your health profile is optimal.

Because I operate entirely as an independent financial blogger and researcher, I do not sell insurance policies, act as an agent, or provide binding coverage quotes. Every individual’s medical profile and financial requirements are completely unique. To find out exactly what your real-time options look like based on your age, geographic location, and current health status, you should check your customized, real-time rates for free using the independent insurance comparison platform Policygenius. They provide a transparent, side-by-side view of top-rated national carriers, making it easy to identify which companies offer the strongest built-in living benefits and the best life insurance riders for chronic illness protection for your specific budget.

Integrating Living Benefits Into a Modern Estate Plan

When building a comprehensive estate plan, the best life insurance riders for chronic illness protection act as a powerful line of defense for your accumulated wealth. Without these living benefits in place, a sudden health crisis in your later years can create a catastrophic domino effect that completely shatters your financial legacy. To see how this fits into broader inheritance goals, review my full guide on the best life insurance for estate planning.

Consider a typical scenario where an individual requires extensive private home health care or specialized memory care services due to a cognitive decline. If their wealth is locked up entirely in real estate, illiquid business assets, or a standard stock portfolio, they may be forced to liquidate those investments rapidly to cover their immediate care costs. Liquidating market assets during an economic downturn can lock in steep losses, and selling real estate in a hurry can trigger massive, unwanted capital gains tax liabilities.

By integrating a policy equipped with the best life insurance riders for chronic illness protection into your estate layout, you introduce an invaluable source of tax-free liquidity exactly when your estate is most vulnerable. The unrestricted cash injections from a chronic illness acceleration can be used to handle immediate medical requirements, hire private aides, or modify your home for safety.

This immediate cash flow allows your core investments, retirement accounts, and family real estate to remain entirely untouched, allowing them to grow quietly and pass smoothly to your designated heirs exactly as you intended. Protecting the generation behind you is much simpler when you utilize the best life insurance riders for chronic illness protection to cover aging vulnerabilities.

A Step-by-Step Guide to Filing a Chronic Illness Acceleration Claim

If the day arrives when you or a loved one must actually execute a claim under a policy’s chronic illness provisions, navigating the administrative process calmly and accurately is critical for securing a swift payout. Insurance companies are highly diligent when verifying claims under the best life insurance riders for chronic illness protection, so staying organized will prevent frustrating delays.

To help you manage this process efficiently, let’s break down the typical step-by-step pathway required to successfully secure your living benefit funds:

1.Notify the Carrier and Request Claim Documents:Initiate within 5 days of a formal diagnosis.

Contact your insurance company’s dedicated living benefits claims department. Formally state that you intend to file a claim under your chronic illness provision and request the comprehensive claim packet, which will include policyholder statements, medical release authorizations, and attending physician statements.

2.Secure Formal Medical Certification:Requires a licensed healthcare practitioner’s sign-off.

Have your primary care physician or a relevant medical specialist complete the detailed attending physician statement. The doctor must explicitly document that you are unable to perform at least two out of the six standard Activities of Daily Living (ADLs) or that you suffer from a severe cognitive impairment requiring continuous supervision. The documentation must state the condition has lasted, or is expected to last, for a continuous period of at least 90 days.

3.Compile and Submit Comprehensive Evidence:Double-check for completeness to avoid administrative loops.

Gather your completed policyholder statements, signed medical release forms, and copies of relevant medical records, diagnostic tests, or prescription logs. Submit the entire, unified packet directly to the carrier’s claims processing center through a secure digital portal or via certified mail.

4.Review the Carrier’s Formal Payout Offer:Typically takes 30 to 60 business days for complete review.

Once the insurer’s medical underwriting team reviews and approves your documentation, they will issue a formal, binding payout offer. This document will outline the exact calculation method they used, the total cash lump sum or monthly per diem they are prepared to send you, and the specific amount that will be permanently deducted from your remaining death benefit. Review these figures carefully with your financial planner or CPA.

5.Accept Funds and Restructure Your Policy:Finalize the transaction and adjust your budget.

Sign and return the acceptance paperwork to finalize your claim. The carrier will distribute your cash via direct deposit or check. Once the funds are released, request an updated policy illustration from the company showing your new, adjusted death benefit and confirming any changes to your future premium obligations.

Common Pitfalls to Avoid When Selecting Coverage

As you evaluate different life insurance policies to find the right fit for your family, you must keep an eye out for hidden traps and subtle contract language that can undermine your protection strategy. Not all chronic illness riders are created equal, and a policy that looks incredibly cheap on the surface might feature highly restrictive terms in the fine print. Searching for the best life insurance riders for chronic illness protection requires checking these fine-print rules.

The Permanency Trap

Many lower-tier chronic illness riders include strict contractual language stating that your health condition must be deemed completely “irreversible” or “permanent” to trigger a payout. If you suffer a major medical event – such as a severe stroke – and your medical team believes there is a chance you might partially recover your functional independence through intensive physical therapy over twelve to eighteen months, a rider with a strict permanency clause will completely deny your claim. Always look for policies that utilize a more flexible 90-day structural expectation rather than an absolute permanency mandate to ensure you own the best life insurance riders for chronic illness protection.

Elimination Periods

Almost every living benefit add-on features an “elimination period” – which is essentially a waiting period that functions like a time-based deductible. A standard elimination period for a chronic illness claim is typically 90 days from the date of medical certification. This means you must independently manage and fund your own care for the first three months of your disability before the insurance company will release a single dollar of your accelerated benefit. You must account for this initial out-of-pocket window when designing your emergency savings buffer.

Capital Caps and Acceleration Limits

Do not assume that having a $1,000,000 life insurance policy automatically means you can access a full $1,000,000 when you become chronically ill. Insurance carriers routinely impose lifetime caps on living benefit accelerations. A policy might limit your total lifetime chronic illness payouts to 50% or 80% of the total face value, or place a hard dollar cap – such as $500,000 – on living benefit payouts regardless of how large the underlying policy is. Verify these internal limits before assuming you have purchased the best life insurance riders for chronic illness protection.

The Long-Term Impact on Your Beneficiaries

As you finalize your research into the best life insurance riders for chronic illness protection, you must maintain a balanced perspective regarding the dual nature of these insurance policies. Every dollar you choose to accelerate and spend on your own medical care or long-term comfort is a dollar that will ultimately be deducted from the legacy sent to your loved ones.

For many families, this trade-off is completely logical and highly efficient. Utilizing your own life insurance policy to cover late-life medical costs prevents you from becoming a financial or physical burden to your children. It allows you to maintain your dignity, control your care environment, and pay for top-tier medical attention using an asset you have already spent years funding.

However, if your primary, non-negotiable financial goal is to provide an exact, guaranteed cash legacy to clear a specific debt – such as a family mortgage – or to fund a specific trust for a dependent grandchild, accelerating your death benefit can disrupt that plan. If you anticipate needing substantial funds for both chronic illness care and a guaranteed legacy, you may want to consider split-funding your strategy by maintaining one core policy dedicated purely to death benefit protection and a separate, secondary policy optimized with the best life insurance riders for chronic illness protection.

Frequently Asked Questions

Can I add a chronic illness rider to an existing life insurance policy?

In most cases, you cannot add a chronic illness rider to a life insurance policy after it has already been active and issued. These living benefits must be selected and undergo underwriting at the time you initially apply for the policy. If your existing policy lacks this protection, your primary options are to replace the policy through a tax-free 1035 exchange or purchase a small, secondary policy that features built-in living benefits. The best life insurance riders for chronic illness protection are always attached during day-one initialization.

Are payouts from a chronic illness rider restricted to medical bills?

No, one of the primary benefits of a qualified chronic illness rider is that the payouts are completely unrestricted. Unlike traditional long-term care insurance policies that require you to submit receipts from licensed care facilities for exact reimbursement, a chronic illness rider pays cash directly to you. You can use this money to pay for experimental treatments, pay off your mortgage, retrofitting your home with accessibility ramps, or even funding a family trip.

What happens to my monthly premium after I execute a claim?

How your premium changes depends entirely on your specific policy contract and the calculation method used by the insurance company. If your carrier uses the Lien Method, your premiums typically stay exactly the same because the payout is treated as a loan balance accumulating interest against the final death benefit. If your carrier uses the Discounted Death Benefit Method, your overall death benefit decreases, and your monthly premium is often reduced proportionally to reflect the lower coverage amount. The best life insurance riders for chronic illness protection will clearly state these terms in your contract.

Can a chronic illness rider be combined with a terminal illness rider?

A history of common, well-managed pre-existing conditions like high blood pressure or mild type 2 diabetes will not automatically disqualify you from securing a policy with a chronic illness rider. Insurance underwriters look closely at your overall stability, treatment compliance, and prescription history. If your readings are consistently within healthy limits through regular medication and you show no signs of secondary organ damage, you can still easily qualify for standard or preferred rates that carry the best life insurance riders for chronic illness protection.

Will a history of high blood pressure disqualify me from getting a rider?

A history of common, well-managed pre-existing conditions like high blood pressure or mild type 2 diabetes will not automatically disqualify you from securing a policy with a chronic illness rider. Insurance underwriters look closely at your overall stability, treatment compliance, and prescription history. If your readings are consistently within healthy limits through regular medication and you show no signs of secondary organ damage, you can still easily qualify for standard or preferred rates that carry the best life insurance riders for chronic illness protection.

Final Thoughts and Next Steps

Securing the best life insurance riders for chronic illness protection is one of the most proactive, intelligent moves you can make to protect your family’s modern financial ecosystem. By transforming a traditional, reactive death benefit into an agile, proactive asset, you ensure that you are fully protected against the financial fallout of a severe health crisis without sacrificing your long-term legacy goals.

Do not wait until a medical diagnosis appears on your permanent health record to start shopping for these protections. Take the time to audit your existing insurance layout, calculate your potential long-term care exposures, and explore your premium options while your health is on your side. Step forward confidently, build a bulletproof financial safety net, and ensure your wealth is thoroughly protected by deploying the best life insurance riders for chronic illness protection.