Buying life insurance for elderly parent coverage simply means purchasing a policy on your mom or dad’s life so that their final expenses, like funeral costs or leftover medical bills, don’t fall on your shoulders or drain the family savings. I learned this the hard way two years ago when my dad casually mentioned he didn’t have “any of that stuff” figured out, and I realized neither did I.

I spent weeks down a rabbit hole of insurance forums, phone calls with agents, and way too many browser tabs. This post is everything I wish someone had handed me on day one.

Table of Contents

Why I Started Looking Into This in the First Place

My dad is 74. He’s healthy, sharp, still drives himself to his weekly bowling league. But after watching a close family friend scramble to cover a $9,000 funeral bill with a credit card, I couldn’t stop thinking about it.

That’s when I first heard the term “final expense insurance” and started piecing together what our options actually were.

My biggest realization during this process was that I had been confusing “life insurance” with one single product. It’s actually a whole category, and the right fit for a 74-year-old looks nothing like a policy for a 35-year-old.

What Buying Life Insurance for Elderly Parent Coverage Actually Involves

Before you call anyone, there are a few concepts you need to understand. These tripped me up at first, so let’s break them down simply.

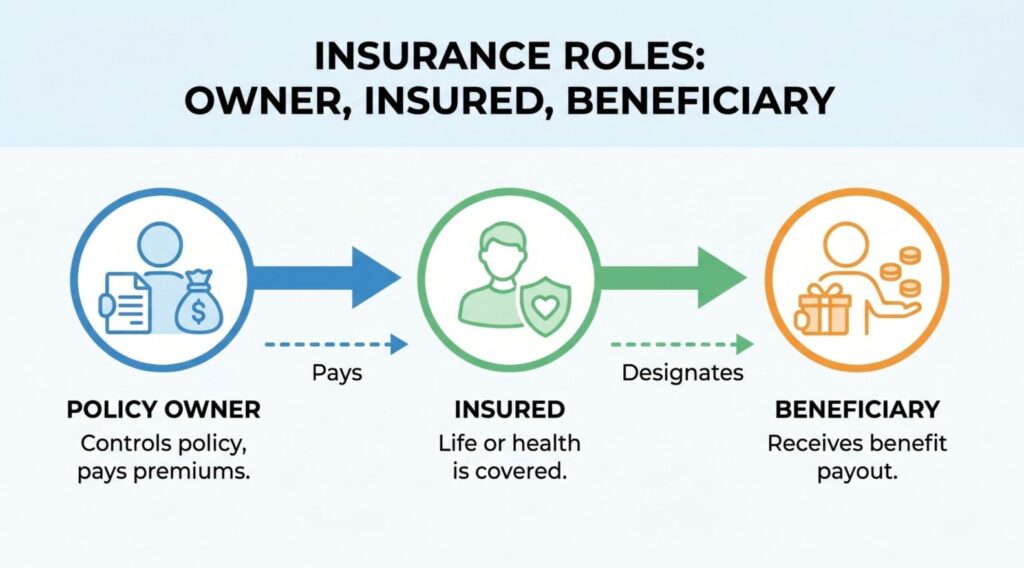

Insurable Interest

You can’t just buy a policy on anyone. Insurance companies require what’s called insurable interest, meaning you need a legitimate financial or emotional stake in that person’s life. As an adult child, you almost always qualify automatically.

Policy Owner vs. Insured

This one confused me for a while. The insured is the person whose life is covered, your parent. The policy owner is whoever controls the policy, pays the premiums, and names the beneficiary. You can be the policy owner even though your parent is the insured, which is actually the setup most adult children choose.

Death Benefit

This is simply the payout amount your beneficiaries receive when your parent passes away. It’s the whole point of the policy, so make sure the number actually covers what you need it to.

The Main Types of Policies I Compared

I narrowed it down to three realistic options for an aging parent. Here’s how they stacked up.

| Policy Type | Best For | Medical Exam Required? | Typical Coverage Amount |

|---|---|---|---|

| Term life insurance for seniors | Healthier seniors under 75 wanting bigger coverage | Sometimes, depends on age and amount | $50,000 to $500,000+ |

| Final expense / burial insurance | Covering funeral and end of life costs | Usually no | $5,000 to $25,000 |

| Guaranteed issue | Seniors with serious health conditions | Never | $5,000 to $25,000 |

A quick note on each:

- Term life insurance for seniors works well if your parent is relatively healthy and you want a larger death benefit, but premiums climb fast with age and coverage often gets harder to find past 80.

- Burial insurance (also called final expense insurance) is built specifically for smaller, predictable costs like funeral homes, caskets, and outstanding medical bills.

- Guaranteed issue policies skip the medical exam entirely, which sounds great, but they come with smaller payouts and higher cost per dollar of coverage.

I genuinely thought skipping the medical exam was always the smarter, easier choice. Turns out guaranteed issue policies usually have a waiting period of two to three years before the full death benefit kicks in for natural causes, so it’s not always the shortcut it seems like.

What Affects the Premium Cost

A few things drive the price up or down, and none of them surprised me more than age. Here’s a rough estimate I put together after comparing several quotes online, just to give you a ballpark.

| Age of Parent | Estimated Monthly Premium (Final Expense, $10,000 benefit) | Estimated Monthly Premium (Term Life, $100,000 benefit) |

|---|---|---|

| 60-65 | $25-$40 | $90-$150 |

| 66-70 | $35-$55 | $150-$250 |

| 71-75 | $50-$80 | Often unavailable or very limited |

| 76-80 | $70-$110 | Rarely available |

| 81+ | $90-$150 | Not typically available |

These numbers vary a lot based on health, gender, and whether a medical exam is involved, so treat this as a starting point, not a quote.

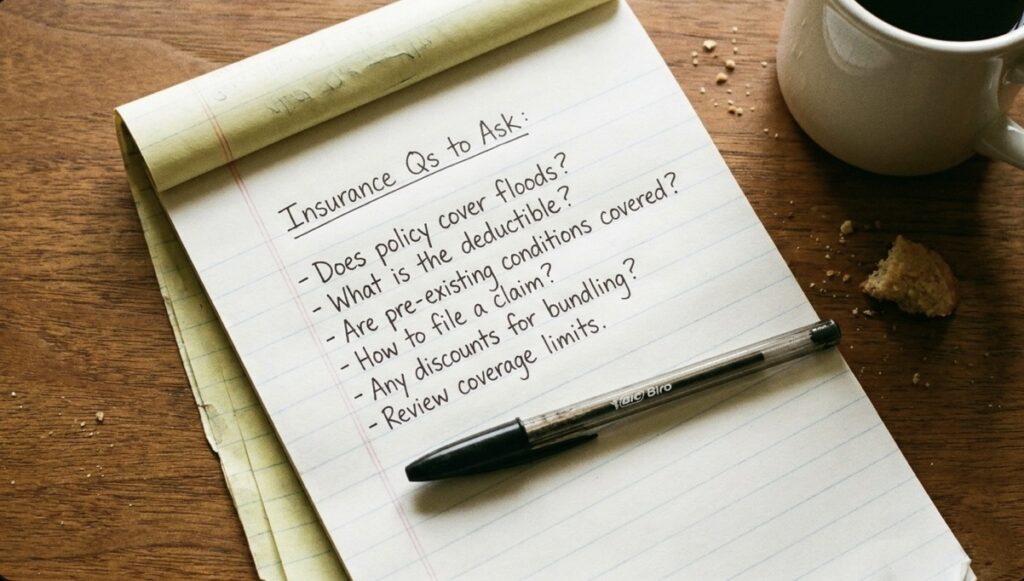

Questions I Asked Before Choosing a Policy

I made a list and basically interrogated every agent I talked to. Here’s what I’d recommend asking too.

- What is the exact death benefit, and does it ever decrease over time?

- Is a medical exam required, and how does that affect the price?

- Is there a waiting period before full benefits apply?

- Can the policy owner be different from the insured person?

- What happens if a premium payment is missed?

- Is the premium locked in for life, or can it increase?

How I Actually Compared Quotes

Honestly, calling individual companies one by one was exhausting and slow. What helped me the most was using a comparison tool that pulled multiple quotes at once so I could see real numbers side by side instead of guessing.

Compare free quotes on Policygenius

I’d recommend doing this early in your research, even before you’ve decided on a policy type, because seeing real pricing makes the whole decision feel a lot less abstract.

A Few Things I Wish I’d Known Sooner

Age and Health Both Matter, Not Just One

I assumed age was the only factor that mattered. Health history, current medications, and even hobbies can shift pricing more than a birthday does.

Smaller Policies Are Often Easier to Qualify For

If your parent has health conditions that complicate term coverage, final expense or guaranteed issue policies tend to have far more lenient approval standards.

Talk to Your Parent Before You Talk to an Agent

This sounds obvious, but I almost skipped it. My dad had opinions about coverage amount and who should be listed as beneficiary that I hadn’t even considered.

Sitting down with my dad before making any calls changed everything. It wasn’t just a financial conversation, it became a moment where we talked openly about what he actually wanted, which felt more meaningful than I expected.

Putting It All Together

If I had to summarize the whole process into a few steps, it would look like this:

- Talk to your parent first about their wishes and comfort level

- Decide whether you need a small final expense policy or a larger term policy

- Check if a medical exam will be required and how that affects pricing

- Compare multiple quotes rather than settling on the first one

- Confirm who the policy owner will be and how premiums get paid

- Read the fine print on waiting periods, especially for guaranteed issue plans

Frequently Asked Questions About Buying Life Insurance for Elderly Parent Coverage

Can I buy life insurance for my elderly parent without them knowing?

No. Every legitimate policy requires the insured person’s knowledge and signed consent, plus proof of insurable interest. Buying life insurance for elderly parent coverage always involves your parent’s direct participation, even if you’re the one handling payments.

What is the maximum age to buy life insurance for a parent?

It depends on the policy type. Guaranteed issue and final expense policies are often available up to age 85 or even older, while term life insurance for seniors typically becomes harder to find past 75 or 80.

Do I need a medical exam to buy a policy for my parent?

Not always. Final expense and guaranteed issue policies usually skip the medical exam entirely, while larger term policies may require one depending on your parent’s age and the coverage amount requested.

Who receives the death benefit?

Whoever is named as the beneficiary on the policy, which the policy owner decides when setting up coverage. This can be you, a sibling, or even a funeral home in some final expense arrangements.

Is buying life insurance for elderly parent coverage worth it if they’re already in poor health?

Often yes, though your options narrow. Guaranteed issue policies exist specifically for this situation, since they don’t require a medical exam, though premiums run higher relative to the death benefit.

One thing that surprised me while buying life insurance for elderly parent coverage was just how many options still existed even after my dad mentioned a couple of health conditions I hadn’t known about. There’s almost always something available, it just takes more digging.

Final Thoughts From One Adult Child to Another

This process felt overwhelming at first, but breaking it into small pieces made it manageable. My dad and I ended up choosing a final expense policy that fit his health situation and our budget, and honestly, just having that conversation brought us closer.

If you’re just starting this journey, take a breath. You’re already doing more than a lot of people do by even researching this.

Again, I’m not a licensed advisor, so please verify details with a professional before signing anything. But I hope walking through my own research saves you some of the confusion I went through.

Quick disclaimer: I’m not a financial advisor, insurance agent, or broker. I’m just a daughter who did a ton of research. Please talk to a licensed professional before making any final decisions for your family.