VA life insurance for seniors is a specialized government benefit program designed to provide financial security and peace of mind to aging veterans and their families, primarily through the Veterans Affairs Life Insurance (VALife) initiative. This program offers guaranteed acceptance whole life insurance to help cover end of life costs.

A few years ago, I found myself sitting at my kitchen table, completely overwhelmed by dozens of open tabs on my browser. I was trying to help my elderly uncle, a proud Army veteran, find dependable coverage to take care of his final expenses. The confusing government portals, endless acronyms, and conflicting guidelines left us both feeling stressed and defeated. That frustrating experience triggered my deep dive into researching options like VA life insurance for seniors so other families would not have to struggle through the same complex web.

Please note a quick and necessary disclaimer before we proceed any further. I am an independent blogger sharing my personal research to help families navigate these choices. I am not a financial advisor, insurance provider, broker, or Department of Veterans Affairs official. This guide is purely for educational purposes, so you should always verify the latest program updates directly with official government sources before making final financial decisions.

Table of Contents

Understanding the Basics of VA Life Insurance for Seniors

When looking into coverage options for older veterans, it helps to understand that the government has modernized its programs significantly. Finding reliable VA life insurance for seniors used to involve strict medical underwriting that disqualified many applicants due to age or health issues. Today, the landscape is much more accommodating for aging heroes who need permanent protection.

The primary solution available today is a permanent program known as VALife. This plan provides guaranteed acceptance whole life insurance, meaning your medical history will not prevent you from getting covered. For senior veterans who have faced medical rejections in the past, this program is a major breakthrough.

It is important to remember that these policies are designed to act as final expense insurance. They provide a modest but reliable payout intended to cover burial costs, outstanding medical bills, or small debts. Securing VA life insurance for seniors ensures that your loved ones are not burdened with these heavy expenses during a time of grief.

What is VALife and Who Qualifies?

The standout option when discussing VA life insurance for seniors is definitely the VALife program. Launched recently to replace older, discontinued programs, VALife simplifies the entire enrollment process for aging veterans. It is tailored specifically to provide accessible protection without making you jump through medical hoops.

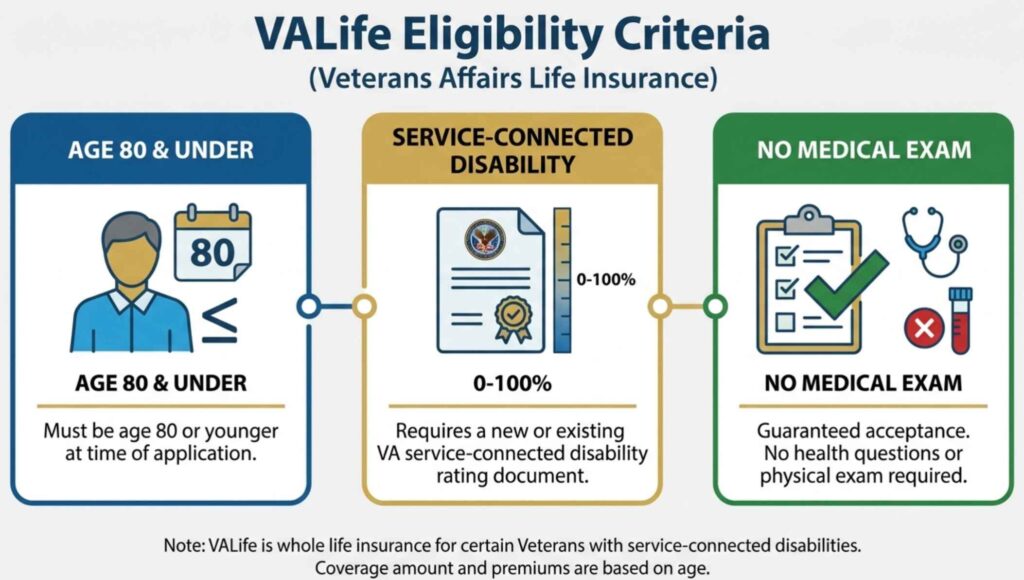

To qualify for this specific type of VA life insurance for seniors, a veteran must meet a few basic criteria. First, you must be age 80 and under at the time you submit your official application. Second, you must have an established service-connected disability rating from the VA, which can range anywhere from 0% to 100%.

If a veteran is over the age of 80, they are typically not eligible for new enrollment in VALife. However, an exception exists if you applied for a service-connected disability rating before turning 81 and received the rating notification later. In that specific scenario, you have a strict two-year window from the date of your rating notice to apply for coverage.

Key Features of the VALife Program

One of the greatest benefits of utilizing VA life insurance for seniors through VALife is the total absence of medical underwriting. You do not have to complete a physical examination, provide blood samples, or answer complex questions about your medical background. Your acceptance is completely guaranteed as long as you meet the age and disability criteria.

The coverage amounts for this program are structured to handle traditional end of life needs. Veterans can select coverage options starting at $10,000 and going up to a maximum of $40,000. This coverage can be selected in clean increments of $10,000 to match your specific budget and final wishes.

Another excellent feature of this type of VA life insurance for seniors is that it builds cash value over time. As you pay your monthly premiums, the policy accumulates a cash component that grows at a fixed rate. This cash value becomes accessible to the policyholder after the policy has been active for a minimum of two years.

The Critical Two-Year Waiting Period

While the guaranteed acceptance nature of VALife is incredibly helpful, there is a major detail you must keep in mind. This type of VA life insurance for seniors features a mandatory two-year waiting period before the full death benefit becomes active. This is a standard practice for insurance plans that do not require a medical exam.

If the insured veteran passes away during this initial two-year window, the beneficiary will not receive the full face value of the policy. Instead, the VA will pay out the total amount of all monthly premiums paid up to that date, plus accumulated interest. This ensures that your money is not lost, even if death occurs early in the policy timeline.

Important Note: The full death benefit of a VALife policy is subject to a strict two-year waiting period. If passing occurs during this time, beneficiaries receive a refund of all paid premiums plus interest rather than the full face value.

Once you successfully cross the two-year mark, the full coverage amount you selected is locked in and fully active. If you are looking at VA life insurance for seniors as a long-term safety net, enrolling as early as possible is the best way to get this waiting period behind you.

[Image Prompt: A clean infographic timeline showing the two-year waiting period for VALife. Year 1 and Year 2 show premium accumulation plus interest refund if death occurs, while the Year 3 marker highlights the full death benefit activation.]

Comparing VALife Monthly Premium Rates

The cost of your monthly premiums is determined entirely by your age at the time you successfully enroll.Because this is a form of permanent whole life insurance, your premium rate will lock in and will never increase as you grow older. This predictable expense makes it much easier to manage on a fixed retirement income.

To help you understand the potential costs, let us look at the estimated monthly premium ranges for older age brackets. The following table illustrates the fixed monthly costs for both a minimum $10,000 policy and a maximum $40,000 policy across several senior milestones.

| Age When You Apply | Monthly Premium for $10,000 Coverage | Monthly Premium for $40,000 Coverage |

| Age 65 | $62.00 | $248.00 |

| Age 70 | $78.00 | $312.00 |

| Age 75 | $99.50 | $398.00 |

| Age 80 | $127.50 | $510.00 |

As you can see from these figures, exploring VA life insurance for seniors earlier in your retirement years yields much lower permanent monthly payments. If you wait until age 80 to secure your plan, the monthly cost reflects the significantly higher risk associated with advanced age.

Veterans Group Life Insurance (VGLI) as an Alternative

Another program often mentioned alongside VA life insurance for seniors is Veterans Group Life Insurance (VGLI). It is vital to recognize that VGLI is fundamentally different from permanent whole life programs like VALife. VGLI is a form of term life insurance that you can transition into after separating from active military service.

While VGLI allows veterans to maintain high coverage amounts up to $500,000, it carries a major drawback for seniors. The premium rates for VGLI are not fixed, meaning they increase significantly every five years based on your age bracket. For older retirees, these escalating costs can eventually make the policy entirely unaffordable.

If you already hold a VGLI policy as a senior, you might find that the premiums are starting to strain your monthly household budget. Many families look into transitioning over to VALife or private final expense insurance to escape those rising costs. Securing a fixed-rate VA life insurance for seniors policy provides long-term financial predictability that term insurance simply cannot match.

Managing Your Policy with a VA Fiduciary

For some elderly veterans, managing monthly bills and insurance details can become difficult due to health challenges or cognitive decline. If a veteran is deemed unable to manage their financial affairs, the VA may appoint a qualified VA fiduciary to step in. This individual is responsible for ensuring that critical benefits and payments are handled correctly.

A VA fiduciary can play a key role in maintaining a policy for VA life insurance for seniors. They can coordinate with the VA to ensure that monthly premiums are automatically deducted from the veteran’s monthly disability compensation or retirement pay. This automatic setup prevents the policy from accidentally lapsing due to a missed payment.

If you are a family caregiver acting as a legal guardian or fiduciary, keeping close track of these insurance records is essential. You can easily manage the VALife policy details online through the secure VA portal or by speaking directly with a designated regional insurance representative.

VALife vs Private Final Expense Insurance

When shopping for final expense coverage, you should never look at government options in total isolation. Many private insurance companies offer competitive whole life plans tailored specifically for seniors. Comparing VA life insurance for seniors against private final expense options will help you find the absolute best value for your hard-earned money.

Private policies often have different eligibility rules, coverage maximums, and underwriting processes. To help you visualize how the VALife program stacks up against typical commercial options, let us look at a direct comparison table.

| Feature Matrix | VALife Program | Private Final Expense Insurance |

| Medical Examination | Never Required | Often Skipped for Simplified Issue |

| Health Questions | No Questions Asked | Required for Better Rates |

| Maximum Coverage | Caps at $40,000 | Can Go Up to $50,000 or More |

| Waiting Period | Strict 2-Year Wait | Varies from 0 to 2 Years Based on Health |

| Premium Structure | Fixed for Life | Fixed for Life |

This table shows that while VALife offers unmatched accessibility for disabled veterans, private insurance might offer faster full coverage if you are in relatively good health. Evaluating these differences is a crucial step in finding the right path forward.

Why You Must Compare VA Rates Against Private Rates

Many people assume that government-sponsored plans will automatically be the cheapest option on the market. However, because VALife accepts every disabled veteran regardless of health status, its premium rates account for a higher overall group risk. If a senior veteran is in good health despite having a minor service-connected disability, private insurance might actually be more affordable.

Private insurance companies reward healthy habits and good medical histories with significantly lower monthly premiums. For example, if your service-connected disability is a localized physical injury that does not impact your overall longevity, a private underwriter might view you very favorably. In that scenario, a private final expense plan could save you thousands of dollars over the lifetime of the policy compared to VA life insurance for seniors.

On the flip side, if a veteran has severe, chronic health conditions alongside their disability rating, private companies will charge extremely high rates or deny coverage altogether. In that situation, the guaranteed acceptance of the VALife program becomes an absolute lifesaver. To make an informed choice, you should always take a few minutes to evaluate your external options.

You can easily explore alternative quotes online to see how they compare to government pricing. Take a moment to Compare free private life insurance quotes on Policygenius. checking these rates side by side ensures you never overpay for your final expense protection.

Steps to Apply for VALife Benefits

If you decide that VALife is the absolute best option for your family, the application process can be completed entirely online. The VA has worked hard to streamline the digital application portal to reduce the type of headaches my uncle and I faced years ago.

- Gather your veteran’s identification details, including their Social Security number and VA file number.

- Ensure you have the official documentation confirming a service-connected disability rating.

- Log into the official VA benefits portal using a verified login method like Login.gov or ID.me.

- Navigate directly to the life insurance section and select the application for the VALife program.

- Choose your desired coverage amount between $10,000 and $40,000.

- Set up your preferred payment method, such as a direct monthly deduction from your VA compensation checks.

Once submitted, the system can often confirm your eligibility and approve the policy within just a few minutes. This rapid automated approval is a massive benefit for families who want to secure a permanent plan without waiting weeks for a manual underwriting decision.

The Value of Permanent Whole Life Protection

Choosing a permanent policy means you are creating a permanent shield for your family. Unlike term policies that expire after a set number of years, a whole life policy remains active for as long as you pay the premiums. This permanence is exactly why so many families seek out VA life insurance for seniors.

Knowing that the policy will not vanish when you hit a certain age milestone brings immense psychological relief. It allows senior veterans to focus on enjoying their retirement years and spending quality time with grandchildren. They can live peacefully knowing that their legacy is fully protected and their final expenses are handled.

Additionally, the steady accumulation of cash value provides an extra layer of financial versatility. While you should never buy a final expense policy purely as an investment vehicle, having that emergency cash reserve can be a comforting backup plan. It represents a tangible asset built through your consistent dedication to your family’s future.

Helpful Tips for Family Caregivers

If you are a family caregiver managing this process for an aging veteran, open communication is your greatest tool. Sit down together and talk openly about final wishes, burial preferences, and funeral costs. Having these difficult conversations today prevents painful guesswork and financial stress down the road.

Always keep a physical copy of the insurance policy documents in a secure, fireproof lockbox at home. Make sure that the primary beneficiary knows exactly where these documents are stored and understands how to initiate a claim. It is also wise to keep a digital copy saved securely in a cloud storage folder for instant access from anywhere.

Caregiver Advice: Always ensure your veteran’s current address and beneficiary designations are updated with the VA. Outdated contact information or old beneficiary names can cause lengthy delays when your family attempts to claim the death benefit.

If the veteran’s health declines significantly, check in regularly with their appointed VA fiduciary or legal representative. Keeping your premium payments completely current is the single most important task to ensure the policy remains in good standing. A lapsed policy can be devastating, especially if the veteran’s age or health has changed since the initial enrollment.

Frequently Asked Questions

Can I keep my VA life insurance for seniors if my disability rating changes?

Yes, once you are successfully enrolled in the VALife program, your coverage is locked in permanently. Even if your service-connected disability rating is later reduced or completely dropped, your policy cannot be canceled by the government. As long as you continue to pay your monthly premiums on time, your permanent whole life protection remains fully active for the rest of your life.

What happens to the cash value if I decide to cancel my policy?

If you choose to surrender your permanent policy after it has been active for at least two years, you are entitled to receive the accumulated cash value. The VA will calculate the total cash component built up in the policy and return that amount directly to you, minus any outstanding administrative adjustments. However, canceling the policy means you forfeit the entire death benefit, leaving your loved ones without final expense protection.

Is there a fast track to bypass the two-year waiting period for VALife?

No, there are absolutely no health exceptions or fast track options available to bypass the mandatory two-year waiting period for VALife. Because the program offers completely guaranteed acceptance with zero medical questions, the two-year rule is applied universally to all applicants. If immediate full coverage is your main priority, you will need to apply for a private life insurance policy that features immediate full day-one benefits through simplified medical underwriting.

How are the death benefits from VA life insurance for seniors taxed?

The death benefit payouts from federal VA life insurance for seniors are entirely exempt from federal income taxation. When your designated beneficiary receives the insurance payout after your passing, they will not have to report that money as taxable income on their tax returns. This tax-free status ensures that the entire face value of your policy goes directly toward handling your final arrangements and supporting your family.

Can a veteran hold both a VGLI policy and a VALife policy at the exact same time?

Yes, a senior veteran is legally allowed to hold both a VGLI policy and a VALife policy simultaneously if they meet the individual requirements for both programs. This combination can be useful if you want to use VGLI for higher temporary coverage while building up a permanent $40,000 foundation with VALife. However, you must ensure that your household budget can comfortably sustain the combined monthly premium payments for both insurance plans.

Who can be named as a primary beneficiary on a VALife policy?

You have complete freedom to name almost anyone as the beneficiary of your choice on a policy for VA life insurance for seniors. This includes your spouse, children, siblings, extended family members, a trusted friend, or even a legal trust. You can also name multiple beneficiaries and split the death benefit percentages among them however you see fit.

How long does it take for the VA to pay out a final death benefit claim?

Once the VA receives the official death certificate and the completed beneficiary claim forms, processing moves relatively quickly. Most uncomplicated claims are reviewed, approved, and paid out within a few weeks. To avoid unexpected delays, family caregivers should ensure that all claim forms are completely filled out with accurate policy numbers and current banking details for direct deposit.

Final Thoughts on Securing Coverage

Navigating the world of senior benefits can feel like a daunting mountain to climb, but you do not have to climb it blindly. Programs like VALife have made securing permanent protection far more attainable for our nation’s aging heroes. By understanding the rules, tracking the timelines, and comparing your options, you can make a choice that truly protects your family.

Take the time to talk with your loved ones, gather your military paperwork, and explore the numbers today. Whether you choose a government-backed plan or a private final expense policy, taking proactive action is the ultimate gift of security for the people you love most. Our senior veterans gave their best to protect our country, and securing the right coverage is a beautiful way to protect their lasting legacy.