Medicare costs and budgeting refers to the systematic process of tracking, projecting, and managing healthcare expenses associated with federal healthcare coverage to protect your retirement savings. Mastering this process is essential for anyone entering retirement or managing a fixed household income. Without a clear plan, unexpected medical fees can quickly disrupt your long-term financial security.

A few years ago, I found myself sitting at my kitchen table, completely surrounded by stacks of medical statements and tax forms. I was trying to help my grandmother map out her healthcare expenses, but the endless stream of numbers left us both completely dizzy. The official federal websites were packed with dense jargon, shifting rules, and hidden structural gaps that made it feel almost impossible to build a predictable household budget. That stressful experience is exactly what inspired me to dive deep into researching Medicare costs and budgeting so other families can avoid the same exhausting confusion.

Please note a quick and necessary disclaimer before we dive into the details. I am an independent blogger sharing my personal research to help families navigate these complex healthcare choices. I am not a Medicare official, insurance provider, broker, or financial advisor. This guide is purely for educational purposes, and you should always verify the latest official rates directly with government resources before making final financial decisions.

Table of Contents

Breaking Down the Core Parts of Medicare

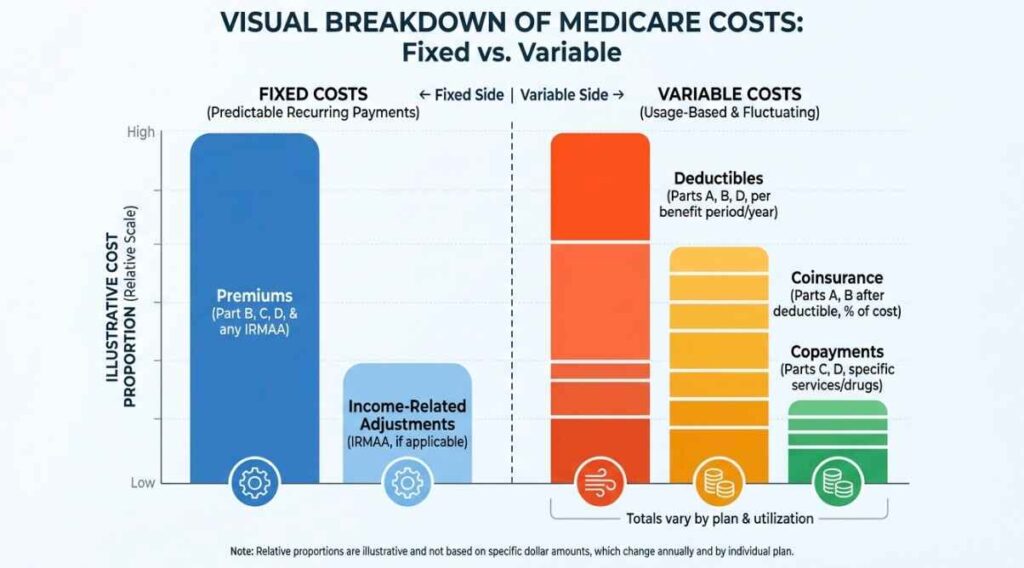

To build an accurate framework for Medicare costs and budgeting, you must first understand the individual components of federal health coverage. Each part covers a specific set of medical services and carries its own separate price tag. Knowing how these pieces fit together prevents you from paying for overlapping coverage or missing vital protection.

Hospital insurance is covered under Part A, which generally handles inpatient hospital stays, skilled nursing facility care, hospice, and some limited home health services. For the vast majority of citizens, this part does not carry a monthly fee because you already paid into the system through payroll taxes during your working years. However, even if your monthly premium is zero, you are still responsible for a significant deductible per benefit period.

Medical insurance is handled under Part B, which covers doctor visits, outpatient care, durable medical equipment, and preventive screenings. Unlike the hospital portion, this medical coverage requires every single enrollee to pay a standard monthly premium. This baseline cost is a foundational element that you must factor into your monthly planning spreadsheet.

Prescription drug coverage is managed through private insurance companies under Part D. Every prescription plan has its own unique list of covered medications and its own separate monthly premium rate. Balancing these specific drug expenses is a critical component of managing your total out-of-pocket expenditures.

The 2026 Medicare Price Sheet

Every single year, the federal government adjusts the baseline fees, deductibles, and premium brackets for the program. Staying updated on these shifting numbers is an absolute requirement for successful Medicare costs and budgeting. The official rates for the 2026 calendar year reflect significant updates that will directly impact your wallet.

To help you map out your upcoming expenses, the following table outlines the standard monthly premium and deductible ranges for each specific segment of your coverage. These figures represent the baseline costs for the current year.

| Medicare Component | Standard Monthly Premium Range | Annual or Per-Benefit Deductible |

| Part A (Hospital) | Usually $0 up to $565 | $1,736 Per Benefit Period |

| Part B (Medical) | Starts at $202.90 | $283 Annually |

| Part D (Prescriptions) | Varies by Plan (Base is $38.99) | Varies (Max Allowed is $590) |

| Medicare Advantage (Part C) | Varies from $0 and up | Varies by Private Carrier |

| Medigap (Supplement) | Varies by Provider and Region | Varies by Plan Letter |

As you review these 2026 figures, notice that the standard Part B premium has adjusted to $202.90 per month. This fixed amount is deducted automatically from your monthly Social Security check if you are already collecting retirement benefits. If you are not yet drawing Social Security, you will receive a direct bill every three months that you must account for in your financial plans.

Understanding Out-of-Pocket Costs

When evaluating Medicare costs and budgeting, focusing entirely on monthly premiums is a very common mistake. The true impact on your retirement nest egg often comes from the hidden variable expenses that occur when you actually use medical services. These expenses include deductibles, copayments, and coinsurance percentages.

A deductible is the initial dollar amount you must pay out-of-pocket before your insurance starts chipping in. For instance, you must pay the first $283 for doctor visits in 2026 before Part B covers the remaining balance. Failing to plan for these initial annual deductibles can lead to a sudden, unexpected cash crunch early in the calendar year.

A copayment is a fixed dollar fee you pay at the time of service, such as twenty dollars for a generic prescription. Coinsurance, on the other hand, is a specific percentage of the total medical bill that you are responsible for paying. Under traditional federal guidelines, you are responsible for a twenty percent coinsurance share for almost all outpatient medical procedures.

The Hidden Surcharges for Higher Earners

If your income during retirement remains relatively high, your Medicare costs and budgeting strategy will look quite different from the standard baseline. The government applies a high-income surcharge known as the Income-Related Monthly Amount, or IRMAA. This surcharge is based on the modified adjusted gross income you reported on your tax returns from two years prior.

For the 2026 plan year, IRMAA brackets begin kicking in if your individual income from two years ago was over $109,000, or over $218,000 for a married couple filing jointly. If you cross these specific tax thresholds, your monthly Part B premium will jump from the standard $202.90 to a significantly higher range. Your Part D prescription premium will also face an additional monthly surcharge that is added directly to your plan base rate.

Important Note: IRMAA surcharges are calculated using your tax records from two years ago. If you experienced a major life-changing event that reduced your current income, such as retirement or divorce, you can file an appeal using Form SSA-44 to lower your premiums.

Failing to anticipate these high-income surcharges can completely wreck your household retirement plan. If you are approaching these income milestones, proactive tax planning is an essential part of effective Medicare costs and budgeting. Working with a professional to manage retirement account withdrawals can help keep your reported income below the surcharge triggers.

Original Medicare vs Medicare Advantage Costs

One of the biggest forks in the road when planning your healthcare budget is deciding between traditional federal coverage and private alternatives. You can choose to stick with Original Medicare, which consists of Part A and Part B, or you can opt for a private bundle known as Medicare Advantage (Part C). Each pathway creates a fundamentally different financial structure for your household.

Original Medicare gives you total freedom to see any doctor in the country who accepts federal insurance, but it features no built-in out-of-pocket maximum. To protect against unlimited twenty percent coinsurance bills, most seniors purchase a separate Medigap policy. This combination creates a predictable budget because your monthly premiums are fixed, leaving you with very little financial surprise.

Medicare Advantage plans operate more like traditional employer health insurance, often featuring very low or even zero-dollar monthly premiums. These private plans bundle your hospital, medical, and prescription coverage into one neat package that includes a mandatory out-of-pocket maximum. However, you must stay within a strict local network of doctors, and you will face various copayments every time you visit a specialist.

| Financial Matrix | Original Medicare with Medigap | Medicare Advantage (Part C) |

| Premium Predictability | High monthly premium costs but no surprises | Low or $0 premiums but variable usage costs |

| Annual Out-of-Pocket Cap | Near zero after meeting your deductibles | Mandatory cap that protects against total ruin |

| Doctor Network Freedom | See any provider nationwide with no referrals | Restricted local networks that require approvals |

| Prescription Integration | Requires a separate Part D standalone plan | Usually bundled into the main private policy |

Choosing the right path is a cornerstone of smart Medicare costs and budgeting. If you prefer paying a higher, predictable monthly amount to ensure you never face unexpected medical bills, the traditional route with a supplement is excellent. If you are in fantastic health and prefer keeping your fixed monthly overhead as low as possible, an advantage plan might fit your lifestyle better.

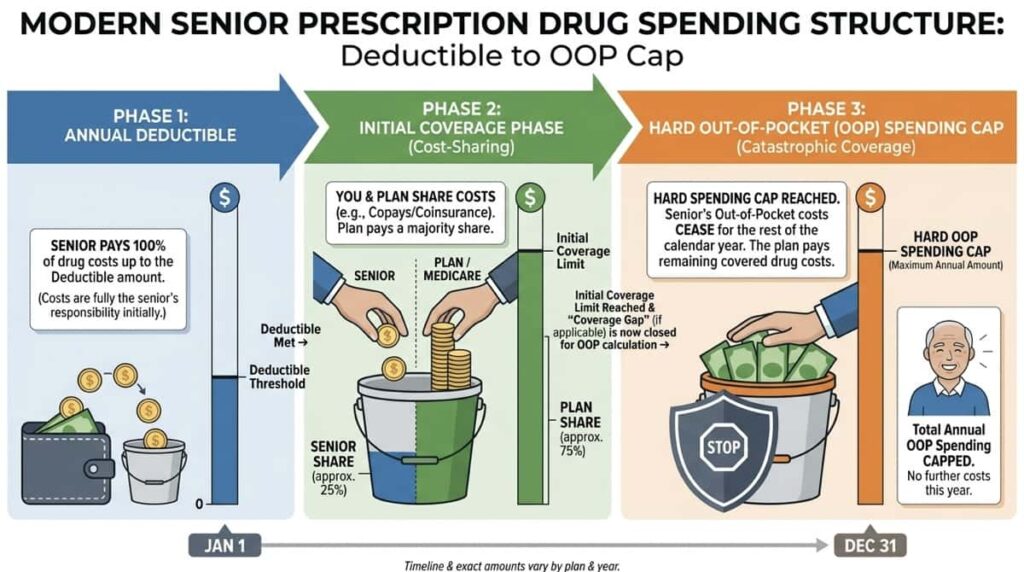

Navigating the Prescription Drug Donut Hole

Managing medication expenses is another major hurdle within the realm of Medicare costs and budgeting. In the past, Part D plans featured a complicated coverage gap commonly referred to as the donut hole. This phase forced seniors to pay a massive percentage of their drug costs out-of-pocket once their total spending hit a specific limit.

Thanks to recent federal legislative overhauls, the structure of prescription drug spending has changed dramatically for seniors. The traditional donut hole has been phased out in favor of a hard cap on all annual out-of-pocket prescription costs. This means that once your total drug expenditures hit the federal ceiling, you pay absolutely nothing for your covered medications for the rest of the year.

Even with these consumer-friendly changes, finalizing your personal Medicare costs and budgeting numbers requires careful annual review. You must make sure that your specific daily prescriptions are included on your chosen plan’s official formulary list. If a critical medication drops off that list, your personal calculation will fluctuate wildly.

The Financial Danger of Late Enrollment Penalties

When mapping out your long-term healthcare strategy, timing is absolutely everything. The federal government enforces strict enrollment windows when you first become eligible for coverage, usually around your sixty-fifth birthday. Missing these specific dates can trigger lifetime financial penalties that are added directly to your monthly premiums.

If you do not sign up for Part B when you are first eligible, your monthly premium could increase by ten percent for each full twelve-month period you delayed enrollment. This penalty lasts for the entire duration of your enrollment, meaning you will pay a higher price for the rest of your life. For a senior living on a tight pension, this lifetime penalty can create a permanent leak in your retirement budget.

Penalty Warning: Late enrollment penalties for Part B and Part D are permanent and compound for every year you delay signing up. Always secure creditable coverage on time to protect your monthly household budget from these lifetime surcharges.

A similar penalty applies to prescription drug coverage if you go without a creditable plan for more than sixty-three consecutive days. The Part D penalty is calculated based on a percentage of the national base beneficiary premium, which changes every year. Avoiding these penalties entirely is one of the easiest ways to keep your Medicare costs and budgeting on track.

Why You Must Compare Private Alternatives

As you build out your comprehensive healthcare budget, it is critical to realize that private insurance costs vary wildly by region and provider. Companies compete aggressively for your business, which means premium rates for identical Medigap or Part D plans can differ by dozens of dollars each month. Shopping around annually during the fall open enrollment period is an absolute necessity.

Reviewing your coverage details every autumn ensures that you are not overpaying for your supplemental or advantage plans. A policy that fit your budget perfectly last year might implement a major premium hike for the upcoming term. Taking a few minutes to evaluate your broader retirement protection plan can save your household thousands of dollars over time.

You can also explore specialized guides like this resource on VA life insurance for seniors to see how military benefits interact with your overall financial strategy. If you are helping an aging relative, it is equally helpful to read about buying life insurance for elderly parent options to ensure no gaps are left in their protective shield. To check alternative rates side by side, take a moment to Compare free private life insurance quotes on Policygenius.

Practical Steps to Build Your Healthcare Budget

Creating a working system for Medicare costs and budgeting does not have to be an overwhelming chore. By breaking the process down into logical, orderly steps, you can eliminate the stress and build an ironclad financial roadmap. Following this systematic routine turns a mountain of confusing paperwork into a clean, predictable line item in your household budget.

- Gather all of your current medical statements, prescription lists, and doctor schedules from the past twelve months.

- Calculate your fixed baseline costs by adding up your annual Part B premiums and any supplemental plan premiums.

- Estimate your variable expenses by reviewing how often you actually visit specialists and tracking your standard copayment rates.

- Identify your maximum financial exposure by checking the out-of-pocket ceiling on your specific advantage or supplement policy.

- Build an emergency healthcare reserve fund to cover your annual deductibles comfortably when they reset each January.

- Set up automatic premium deductions from your monthly benefits check to prevent any accidental coverage lapses.

Frequently Asked Questions About Medicare costs and budgeting

Does Medicare cover the cost of long-term nursing home care?

Traditional federal health coverage does not pay for custodial, long-term nursing home care or assisted living facilities. Part A will only cover limited, short-term stays in a skilled nursing facility for rehabilitation after a qualified inpatient hospital stay. For long-term care needs, seniors must rely on private long-term care insurance, personal savings, or qualify for state Medicaid assistance.

Can I change my coverage choices if my health changes mid-year?

Generally, you can only modify your specific plan choices during the official annual Open Enrollment Period, which runs from October 15 through December 17 each year. If you experience a major qualifying life event, such as moving to a new state or losing employer coverage, you may trigger a Special Enrollment Period. Outside of these official windows, your coverage choices are locked in for the remainder of the calendar year.

What happens to my healthcare budget if my doctor drops out of my network?

If you are enrolled in a private advantage plan and your preferred doctor leaves the network mid-year, you will generally have to find a new in-network provider to keep your lower copayment rates. Seeing an out-of-network doctor can result in significantly higher out-of-pocket fees or a complete denial of payment. This network risk is a major factor that you must weigh carefully when executing your personal Medicare costs and budgeting.

Is dental, vision, and hearing care covered under the standard premiums?

Original federal coverage under Parts A and B does not include routine dental cleanings, vision exams, eyeglasses, or hearing aids. To secure these specific benefits, many seniors choose to enroll in private advantage plans that include routine wellness bundles. Alternatively, you can purchase standalone private dental and vision policies to keep these common expenses separate from your core medical budget.

How does the Hold Harmless Rule protect my Social Security income?

The Hold Harmless Rule is a federal consumer protection regulation that prevents your net Social Security benefit from decreasing due to Part B premium hikes. If the annual cost of living adjustment for Social Security is very low, the government cannot raise your premium by an amount that reduces your monthly check below the previous year’s level. This rule provides fantastic protection for lower-income retirees who rely entirely on their monthly government checks.

Should I keep my employer group health insurance after turning sixty-five?

If you are still actively working at age sixty-five and your employer has twenty or more employees, your group health insurance can usually act as your primary coverage. In this specific scenario, you can safely delay enrolling in Part B without facing any late enrollment penalties down the road. This delay allows you to avoid paying the monthly premium until you officially retire from the workforce.

How do I apply for financial help if I cannot afford my premiums?

Seniors with limited monthly income and minimal personal assets can apply for state assistance through Medicare Savings Programs. These government programs can help pay for your monthly Part B premiums, annual deductibles, and various coinsurance fees. You can also apply for the federal Extra Help program, which provides significant financial assistance to lower the cost of your daily prescription medications.

Final Thoughts on Smart Planning

Mastering your healthcare numbers takes patience, but the long-term peace of mind is worth every single ounce of effort. By taking control of your financial planning today, you are building a safe harbor for your retirement years. You do not have to let confusing government portals or rising medical fees dictate your financial future.

Take the time to organize your medical paperwork, review your plan structures annually, and explore private alternatives to maximize your savings. Protecting your health and your hard-earned savings is one of the most proactive steps you can take for your family. With the right strategy in place, you can confidently step into your golden years knowing that both your wellness and your wealth are beautifully secure.