Can you qualify for final expense insurance with health issues is a common question for families looking to secure permanent whole life protection to cover end of life costs despite a history of medical conditions. This type of specialized coverage is specifically designed to accept applicants who might be rejected for traditional policies due to their age or physical wellness. It offers a straightforward way to build a financial safety net so your loved ones are not left with a heavy burden.

A few years ago, I found myself sitting at my kitchen table, completely overwhelmed by dozens of open browser tabs. I was trying to help my grandmother find an affordable policy to cover her burial costs, but her chronic diabetes and high blood pressure made every application seem like a dead end. The confusing questionnaires and sudden rejections left us both feeling stressed and entirely defeated. That frustrating experience is exactly why I decided to thoroughly research how can you qualify for final expense insurance with health issues so other families would not have to face the same exhausting roadblocks.

Please note a quick and necessary disclaimer before we proceed any further. I am an independent blogger sharing my personal research to help families navigate these choices. I am not a financial advisor, insurance provider, broker, or government official. This guide is purely for educational purposes, so you should always verify the latest guidelines and rates directly with individual carriers before making final financial decisions.

Table of Contents

How Health Conditions Impact Your Coverage Options

When people ask can you qualify for final expense insurance with health issues, they are often relieved to learn that medical underwriting for these plans is incredibly lenient. Traditional life insurance requires exhaustive physical exams, blood draws, and decades of medical records. Final expense insurance completely skips the physical checkups, focusing instead on simplified questionnaires or offering guaranteed approval.

Your options will generally fall into two main pathways based on the severity of your current medical conditions. Healthy seniors or those with well-managed conditions can apply for simplified issue plans. These plans feature a short list of health questions but skip the physical exams entirely.

For individuals with more severe diagnoses, guaranteed acceptance whole life insurance provides an absolute safety net. With this option, there are no medical questions asked and approval is completely guaranteed regardless of your medical past. Understanding these two pathways is the secret to answering can you qualify for final expense insurance with health issues.

Simplified Issue Policies for Managed Conditions

If you are wondering can you qualify for final expense insurance with health issues that are stable and controlled, a simplified issue policy is usually your best route. Insurance companies routinely approve applicants dealing with common age-related health conditions. As long as your conditions are managed with standard medications, you can easily secure day-one protection.

- High blood pressure and high cholesterol are almost universally accepted by final expense underwriters.

- Controlled Type 2 diabetes without severe complications typically qualifies for standard rates.

- Mild asthma or well-managed depression will rarely cause an application to be rejected.

Securing a simplified issue policy means you get full coverage from the very first day your policy goes active. This means your beneficiaries will receive the full face value if passing occurs at any point. It is the most affordable way to resolve the question of can you qualify for final expense insurance with health issues.

Guaranteed Issue Policies for Severe Health Issues

For families facing much more serious medical challenges, the question becomes even more urgent. If a senior is dealing with advanced illnesses, a guaranteed issue policy is the definitive answer to can you qualify for final expense insurance with health issues. These plans completely eliminate the health questionnaire from the application process.

- Advanced dementia or Alzheimer’s disease can be fully covered under a guaranteed plan.

- Patients currently undergoing active cancer treatments are automatically approved.

- Individuals on kidney dialysis or relying on 24-hour oxygen tanks face zero medical barriers.

Because the insurance company accepts a massive amount of risk by skipping health questions, these plans feature a unique structure. They protect the carrier by utilizing a mandatory waiting period before the complete death benefit becomes active. Knowing this distinction is essential when exploring can you qualify for final expense insurance with health issues.

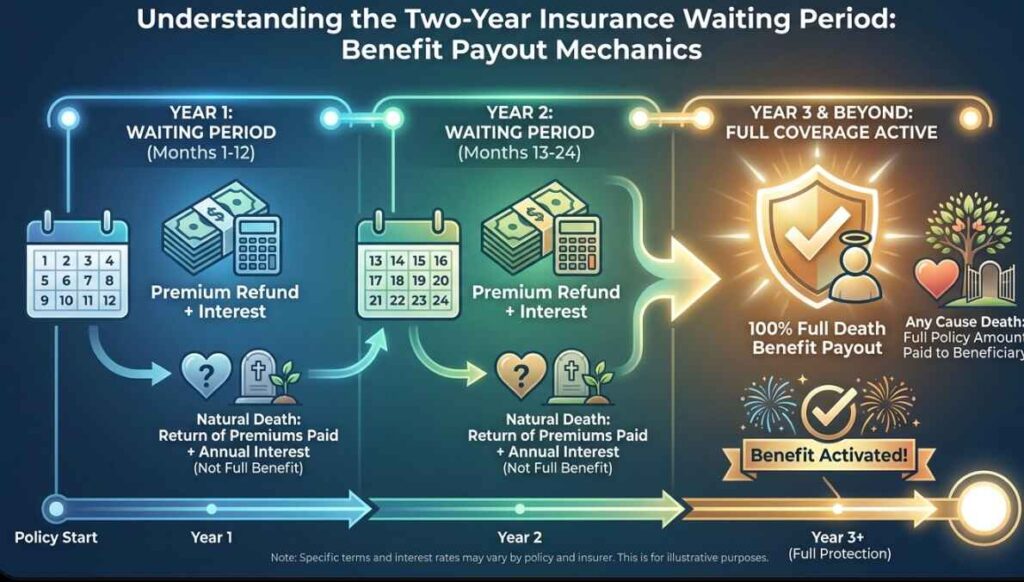

The Critical Two-Year Waiting Period

When you look into can you qualify for final expense insurance with health issues through a guaranteed plan, you must account for the two-year waiting period. If the insured individual passes away from natural causes during these initial twenty-four months, the full policy value is not paid out. Instead, the company issues a complete refund of all monthly premiums plus a fixed interest rate.

Important Advice: The mandatory two-year waiting period is a standard safety feature for all guaranteed issue plans. If a senior passes away from natural causes during this window, beneficiaries receive a full refund of paid premiums plus interest rather than the full face value.

Once you successfully cross that two-year milestone, the entire death benefit is locked in and fully active. If passing occurs after this period, the full payout goes directly to your beneficiaries tax-free. This timeline is an important factor to consider when determining can you qualify for final expense insurance with health issues early.

Estimating Your Monthly Premium Costs

The permanent monthly cost of your final expense policy is determined by your age, gender, and tobacco usage at enrollment. Because these are permanent whole life plans, your premium rate will lock in and will never increase as you grow older. This fixed expense makes it incredibly easy to manage alongside a set monthly retirement income.

The following table outlines the estimated monthly premium ranges for final expense insurance based on common older age brackets. These numbers demonstrate the typical costs for both a modest $10,000 policy and a larger $40,000 policy.

| Age When You Apply | Monthly Premium for $10,000 Policy | Monthly Premium for $40,000 Policy |

|---|---|---|

| Age 65 | $45.00 to $65.00 | $180.00 to $260.00 |

| Age 70 | $55.00 to $85.00 | $220.00 to $340.00 |

| Age 75 | $75.00 to $115.00 | $300.00 to $460.00 |

| Age 80 | $100.00 to $165.00 | $400.00 to $660.00 |

Reviewing these numbers highlights why starting the process early is so beneficial to your long-term budget. Waiting until advanced age causes the permanent monthly rates to climb significantly. This table provides a clear financial perspective on how can you qualify for final expense insurance with health issues at a manageable price.

Special Options for Senior Veterans

If the senior in your family is a military veteran, you have access to specialized government programs that change the conversation entirely. When veterans ask can you qualify for final expense insurance with health issues, they should immediately look into the VALife program. This initiative was created specifically to support those who served our nation.

The VALife program provides guaranteed acceptance whole life insurance to veterans with an established service-connected disability rating. Applicants must be age 80 and under to qualify for standard enrollment windows. Like private guaranteed plans, it features a strict two-year waiting period but requires absolutely no medical examinations.

Some older veterans might confuse this with Veterans Group Life Insurance (VGLI), which is a term life program. VGLI premiums increase significantly every five years, which can make it hard to maintain on a fixed income. For permanent protection that builds cash value, VALife is an excellent answer to can you qualify for final expense insurance with health issues.

If a veteran faces cognitive challenges, a designated VA fiduciary can easily step in to manage the policy details. The fiduciary can arrange for monthly premium payments to be deducted automatically from the veteran’s monthly compensation checks. This simple organizational setup ensures that the vital coverage never accidentally lapses.

Securing Coverage for an Elderly Parent

Many adults research can you qualify for final expense insurance with health issues while trying to protect their aging parents. Taking care of Mom or Dad often means stepping in to handle their end of life planning. You can easily manage this process as long as you have their direct consent and participation.

If you want to read a deeper guide on managing this family milestone, check out this comprehensive breakdown on buying life insurance for elderly parent situations. It outlines the legal requirements and conversational strategies needed to establish coverage smoothly. It is a perfect companion piece for anyone asking can you qualify for final expense insurance with health issues.

To see how these private final expense strategies stack up against specialized veteran benefits, you can also explore this detailed article on VA life insurance for seniors programs. Comparing these different pathways ensures you do not miss out on valuable federal assistance. It gives you a complete view of every available financial tool.

VALife vs Private Final Expense Insurance

When finalizing your family strategy, comparing government plans against commercial alternatives is a critical step. Private providers often offer different maximum coverage amounts and distinct health niches. This comparison matrix highlights the key operational differences you will encounter.

| Evaluation Metric | VALife Government Program | Private Final Expense Plans |

|---|---|---|

| Medical Examination | Never Required | Completely Skipped |

| Maximum Face Value | Maximum of $40,000 | Can Reach $50,000 or More |

| Health Screenings | No Health Questions Asked | Questions Required for Better Rates |

| Waiting Period Structure | Universal 2-Year Waiting Period | Varies from 0 to 2 Years Based on Answers |

| Cash Value Accumulation | Builds Slowly Over Time | Builds Steadily at Fixed Rates |

This comparison shows that private plans can sometimes offer immediate full coverage if your health issues are relatively minor. However, for severe chronic illnesses, the government program remains an incredibly stable choice. This matrix is a useful tool for visualizing how can you qualify for final expense insurance with health issues across different sectors.

Why You Must Compare Rates Prior to Enrolling

Many people assume that final expense prices are identical across the industry, but this is a major misconception. Every private insurance company utilizes its own proprietary underwriting manual to evaluate medical conditions. A health issue that causes one company to issue a denial might be completely ignored by a competing carrier.

Shopping around allows you to find the specific provider that treats your unique medical history most favorably. This can mean the difference between paying high guaranteed issue rates or qualifying for low simplified issue pricing. Taking this extra step protects your retirement savings from unnecessary monthly leaks.

To get a clear look at your external commercial options, it is wise to utilize modern online quoting tools. Take a few minutes to Compare free private life insurance quotes on Policygenius. mapping out these numbers side by side guarantees that you secure the absolute best market value. It gives you the empirical data needed to resolve can you qualify for final expense insurance with health issues confidently.

Practical Steps to Apply for a Policy

Ready to secure a final expense plan for your family? Following an orderly sequence simplifies the entire application process and eliminates unwanted stress. This step-by-step routine ensures that your application is processed quickly and accurately.

- Compile a complete list of all current prescriptions, medical dosages, and official health diagnoses.

- Determine your target coverage amount by calculating local funeral, burial, or cremation costs.

- Decide whether your medical history requires a guaranteed issue plan or fits a simplified issue plan.

- Gather the social security numbers, birth dates, and contact details for your chosen primary beneficiaries.

- Submit your application online or over the phone with a licensed agent to receive a rapid decision.

- Establish an automatic bank draft for premium payments to ensure the policy remains continuously active.

This systematic approach takes the mystery out of the application journey. It transforms a complex financial chore into a straightforward task that you can finish in a single afternoon. It is the ultimate roadmap for answering can you qualify for final expense insurance with health issues.

Caregiver Advice: When filling out health questionnaires, always be completely honest about all pre-existing medical conditions. Misrepresenting a health issue can lead to a denied claim later, completely defeating the purpose of buying the policy.

Frequently Asked Questions

Can you qualify for final expense insurance with health issues like recent heart surgery?

Yes, you can easily qualify for coverage even if you have undergone recent heart surgery. If the surgery occurred within the last twelve to twenty-four months, you will likely be directed toward a guaranteed issue policy that features a two-year waiting period. If the surgery occurred many years ago and your heart health is completely stable, you may even qualify for a simplified issue plan with immediate day-one benefits.

What happens to my monthly premium if my health declines after buying the policy?

Once your final expense policy is officially approved and active, your monthly premium rate is permanently locked in for life. The insurance company cannot raise your monthly bill or cancel your coverage if you are diagnosed with a new illness later. As long as you pay your premiums on time, your permanent protection remains entirely secure regardless of changes in your physical wellness.

Can a senior hold multiple final expense policies from different companies?

Yes, a senior is legally allowed to own multiple final expense policies from different insurance carriers at the same time. This strategy is often used by families who want to piece together small increments of coverage to reach a specific financial goal. You must simply ensure that your combined monthly premiums fit comfortably within your household retirement budget.

Does final expense insurance build a accessible cash value over time?

Yes, because final expense policies are structured as permanent whole life insurance, they accumulate a small amount of cash value over time. A portion of each monthly premium payment is funneled into a fixed-rate cash reserve that grows steadily over the lifespan of the policy. Policyholders can eventually borrow against this cash value if an emergency financial need arises during their retirement years.

How do beneficiaries file a claim after the insured individual passes away?

Filing a final claim is a very straightforward process that can be completed within a few business days. The primary beneficiary must contact the insurance company directly to request the official claim forms and submit a certified copy of the death certificate. Once the paperwork is verified, the carrier issues the death benefit payout directly to the beneficiary as a tax-free lump sum.

Are there any specific age limits for guaranteed issue final expense plans?

Most private insurance companies offer guaranteed issue final expense plans to applicants between the ages of 50 and 85. If you fall within this traditional age bracket, your approval is completely guaranteed regardless of your medical background. If you are over the age of 85, your options become much more limited, making it critical to establish coverage before hitting that milestone.

What is the primary difference between burial insurance and final expense insurance?

Burial insurance and final expense insurance are actually two different names for the exact same financial product. Both terms refer to a small, permanent whole life insurance policy designed specifically to cover end of life costs, medical bills, and funeral services. The payout is delivered directly to your beneficiaries as cash, giving them total freedom to use the funds however they need.

Final Thoughts on Securing Peace of Mind

Answering the question of can you qualify for final expense insurance with health issues brings immense relief to families across the country. The insurance market has evolved to ensure that aging seniors are never left without a dependable safety net. You do not have to let past medical rejections or complex health challenges stop you from protecting your family.

Take the time to review your options, talk openly with your parents, and compare multiple rates to maximize your household savings. Securing a permanent final expense plan today is a powerful act of love that removes financial stress from your family’s future. With the right policy in place, you can move forward confidently knowing that your loved ones are completely shielded and your legacy is perfectly secure.