Can an 80 year old get life insurance? Yes, an 80-year-old can absolutely secure a life insurance policy, though the core purpose of the coverage shifts significantly from income replacement to managing immediate final end-of-life exposure. If you are shopping for yourself or trying to figure out the logistics of buying life insurance for an elderly parent, navigating this landscape can feel overwhelming. Many wonder if a senior can qualify, or ask: can an 80 year old get life insurance without excessive premium hikes? Fortunately, specialized products exist specifically tailored to this demographic.

Three years ago, I sat at a kitchen table with my Aunt Martha, who was 83 at the time. Her old 20-year term insurance policy had quietly expired on her 80th birthday, leaving her with absolutely zero coverage. She was panicked, believing that her age made her entirely uninsurable and kept asking me, “can an 80 year old get life insurance at this stage in life?” Digging into the options taught us that while the rules are strict and the pricing is higher, affordable protection is within reach if you know where to look.

Table of Contents

Understanding Your Choices: Term Life Insurance Over 80 vs. Permanent Policies

When exploring your options, the central question changes from “can an 80 year old get life insurance?” to “what type of coverage actually makes financial sense?” The type of plan you choose directly impacts both monthly costs and long-term financial security.

Term Life Insurance Over 80

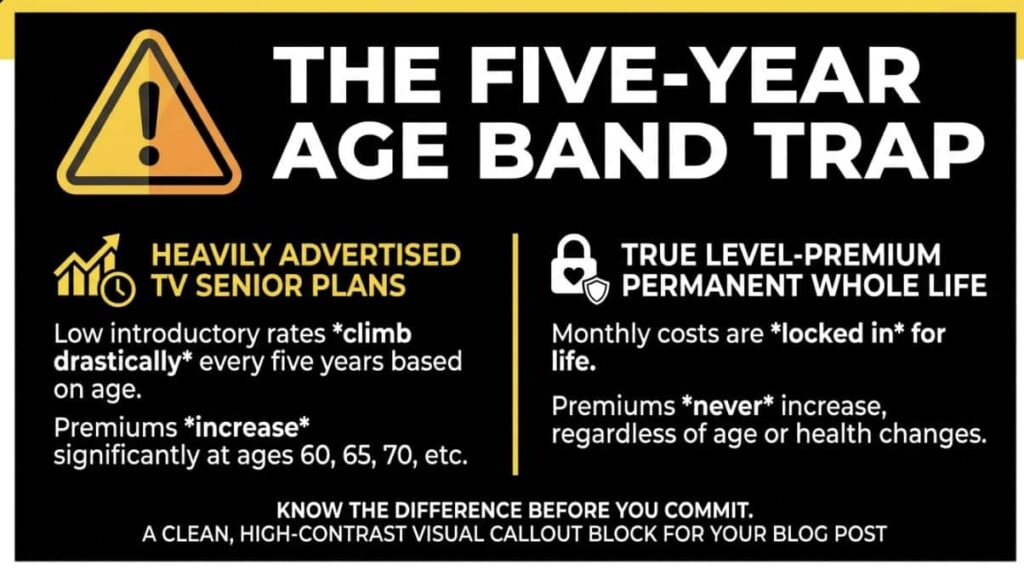

Traditional term life insurance over 80 is rarely advisable, and often entirely unavailable. When families ask if a senior can buy a standard policy, they quickly find that most highly rated companies enforce a strict maximum issue age cap for new term policies, typically cutting off applications at age 75 or exactly age 80.

Even if you manage to locate a carrier offering a short 5-year or 10-year term policy at age 80, the premiums are astronomically high. More importantly, term insurance has a fixed expiration date. If the insured outlives the term, the policy terminates with no payout, meaning you will face the exact same question again: can an 80 year old get life insurance once a term plan expires?

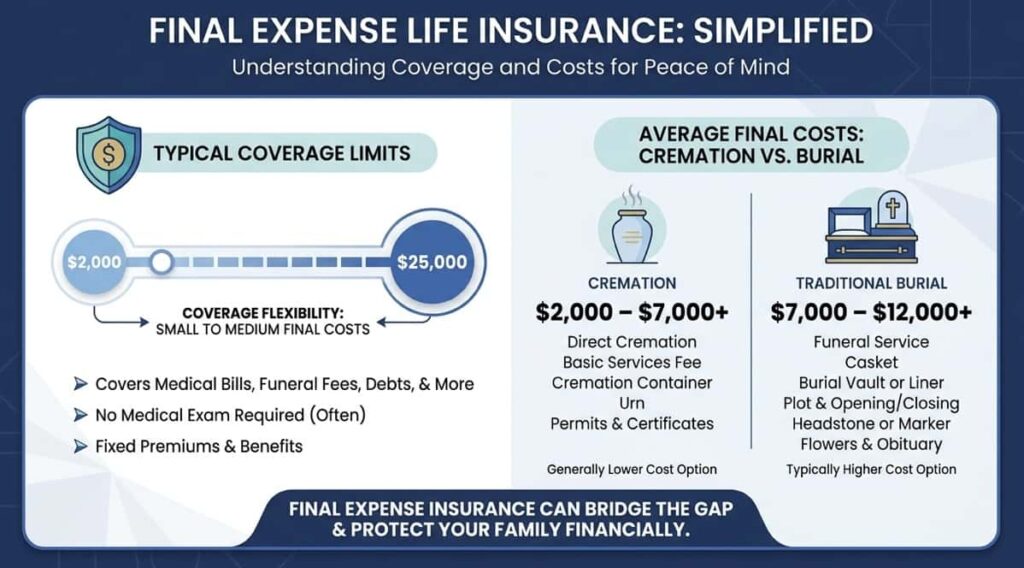

Final Expense Life Insurance

For the vast majority of octogenarians, final expense life insurance (often referred to as burial insurance or funeral insurance) is the most logical path. When considering how a parent can qualify, these small whole life insurance policies are specifically designed to handle end-of-life bills, outstanding medical debts, and legal fees. Unlike term coverage, final expense policies are permanent: they build cash value over time, their monthly premium rates are permanently locked in, and the death benefit is guaranteed never to decrease as long as premiums are paid.

Guaranteed Universal Life Insurance (GUL)

If you require a coverage amount larger than a standard final expense policy (which usually caps out at $25,000 or $50,000), a Guaranteed Universal Life Insurance policy acts as a highly effective bridge. So, if you are asking can an 80 year old get life insurance with a higher face value?, GUL is often the answer. It functions similarly to a permanent, non-expiring term policy that can be dialed in to last until age 90, 95, or even age 121. It provides a pure, no-frills death benefit without the complex cash-value accumulation elements of standard whole life, keeping premiums slightly more competitive for higher coverage sums.

Simplified Issue vs. Guaranteed Issue: The Underwriting Crossroads

A senior’s current medical profile dictates the underwriting tier they qualify for, which determines whether the policy pays out immediately or requires a waiting period. If you are asking can an 80 year old get life insurance with pre-existing conditions?, understanding this crossroads is essential.

Simplified Issue Life Insurance

A simplified issue policy does not require a physical medical exam or blood work. Instead, the application relies on a brief “Yes/No” health questionnaire alongside an automated check of prescription drug history databases. If the applicant can truthfully answer “No” to major chronic or terminal health questions, they can secure first-day full coverage.

Guaranteed Issue Life Insurance

For individuals dealing with severe, unmanaged health conditions, a guaranteed issue whole life for seniors 80and older provides an absolute safety net. When families ask can an 80 year old get life insurance after a heart attack or stroke?, a guaranteed plan ensures approval. These policies feature zero health questions and no medical background checks. Approval is fully guaranteed regardless of pre-existing conditions, making it an accessible option for seniors who are otherwise uninsurable.

“The absolute biggest mistake consumers make when shopping for an elderly relative is assuming that a history of moderate health issues like controlled Type 2 diabetes forces them into a guaranteed acceptance plan. This misunderstanding automatically subjects them to higher rates and a mandatory waiting period that they could have easily avoided with proper simplified underwriting navigation.”

The Reality of the 2-Year Waiting Period Caveat

Every single guaranteed issue policy sold in the United States features a mandatory two-year graded death benefit waiting period. If you are asking can an 80 year old get life insurance with no waiting period?, you must bypass guaranteed acceptance and pass a basic simplified health questionnaire instead. Insurance companies enforce this rule to protect themselves from insuring individuals who are already terminal.

- Natural Causes (Months 1-24): If the insured passes away from natural causes (such as an illness, stroke, or heart attack) during the first 24 months, the policy does not pay out the face value. Instead, the company provides a full return of all paid premiums plus an additional interest payout (typically 10%).

- Accidental Causes (Day 1+): If death occurs due to a verifiable accident (such as a car crash or a fall) at any point after the policy is active, the two-year rule is completely bypassed, and the beneficiary receives 100% of the full death benefit immediately.

- Post-Month 24: Once the policy crosses the 24-month mark, the full death benefit unlocks completely for all causes of death.

To ensure you aren’t overpaying or getting trapped in an unnecessary waiting tier, it is critical to avoid the most common mistakes to avoid in life insurance for seniors over 80, such as accepting a graded policy when a simplified option was entirely possible.

What Does a $10,000 Policy Cost for an 80-Year-Old?

Insurance companies determine premium rates based heavily on actuarial life expectancy tables. Because women statistically live longer than men, men face higher monthly premium rates at this age bracket. When researching can an 80 year old get life insurance at an affordable rate?, reviewing these tables can help you establish a realistic baseline budget.

Estimated Monthly Premiums for Men (Non-Tobacco)

| Age | $5,000 Death Benefit | $10,000 Death Benefit | $25,000 Death Benefit |

| 80 | $70.00 | $133.00 | $334.00 |

| 82 | $79.00 | $151.00 | $382.00 |

| 85 | $110.00 | $210.00 | $525.00 |

Estimated Monthly Premiums for Women (Non-Tobacco)

| Age | $5,000 Death Benefit | $10,000 Death Benefit | $25,000 Death Benefit |

| 80 | $48.00 | $98.00 | $235.00 |

| 82 | $58.00 | $116.00 | $280.00 |

| 85 | $82.00 | $158.00 | $395.00 |

Best Life Insurance Companies for Seniors Over 80

When shopping for coverage, focusing on companies with high financial stability ratings and clear senior-market products is essential. Thoroughly comparing quotes and policies of life insurance over 80 will reveal that underwriting standards vary wildly between major names:

- Mutual of Omaha: Highly recommended for simplified issue permanent plans. They accept applicants up to age 85, offer competitive rates, and provide true first-day full coverage if you pass their basic medical questionnaire.

- AARP / New York Life: A deeply popular option among seniors. They offer permanent whole life insurance up to age 80 for members, featuring fixed rates that lock in for life.

- Gerber Life: Widely known for their guaranteed issue whole life insurance. They offer easy, no-questions-asked approval for seniors up to age 80, making them an excellent backup option if health issues rule out simplified underwriting.

As an independent blogger, I am not an insurance provider or broker. I highly recommend cross-referencing any carrier you are considering with the National Association of Insurance Commissioners (NAIC) or A.M. Bestto freely verify their financial strength ratings and consumer complaint indexes before making a choice.

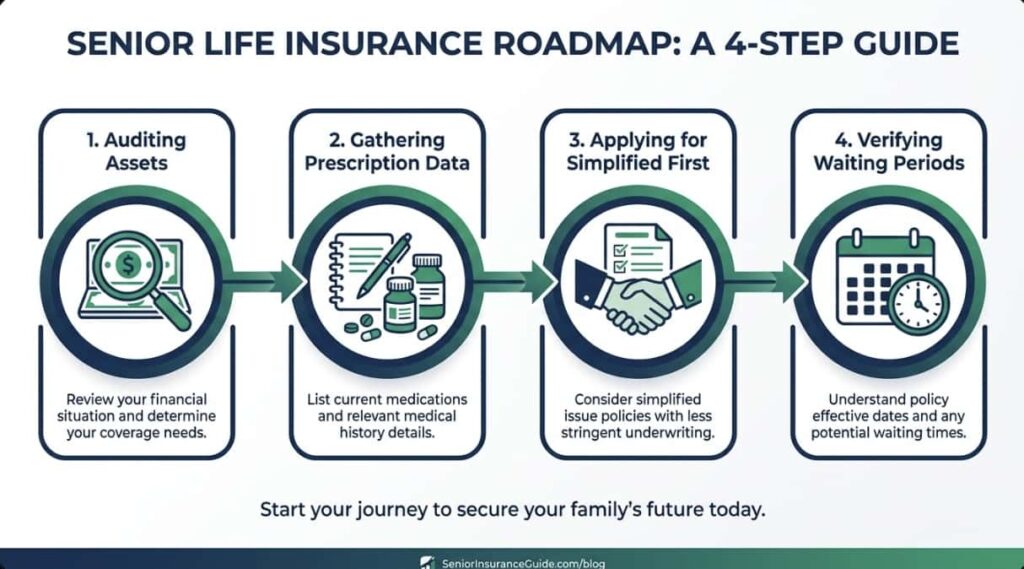

Step-by-Step Guide to Securing Coverage Wisely

If you are ready to explore your options and want to answer the practical question, how can an 80 year old get life insurance efficiently?, following a structured process helps ensure you locate the right policy at a price that fits your budget.

- Audit Existing Legacy Assets: Review any past workplace coverages, active paid-up whole life policies, or existing savings accounts to calculate the exact remaining financial gaps for your final arrangements.

- Document All Current Prescription Histories: Compile an accurate list of all active medications, dosages, and formal diagnoses. This information is critical for answering simplified issue questionnaires correctly.

- Prioritize Simplified Underwriting Pathways: Always apply for a policy that asks health questions first. Only pivot to a guaranteed issue option if explicit medical conditions create an absolute barrier to standard underwriting approval.

- Verify the Exact Policy Delivery Provisions: Confirm whether the contract contains an immediate first-day full death benefit or if it mandates a graded structural waiting tier before signing.

Senior Insurance FAQ

Can an 80 year old get life insurance without their child initiating the process?

Yes, any mentally competent 80-year-old can apply for their own coverage. However, many adult children initiate the process to protect themselves from inheriting future funeral debt. While you can legally pay the monthly premiums and act as the policy owner, the insured parent must participate, answer health questions, sign the application documents, and provide explicit consent.

What is the absolute maximum age cutoff to buy a new life insurance policy?

In the 2026 market, most highly rated carriers enforce a strict application cutoff between ages 85 and 89 for final expense whole life plans. Once a senior turns 90, traditional on-market life insurance options are virtually non-existent. At that stage, alternative vehicles like irrevocable funeral trusts or dedicated savings accounts become the only viable methods for pre-funding final expenses.

Does a senior’s smoking status impact premium rates as severely at age 80?

Yes, tobacco usage still triggers a noticeable premium surcharge, but the gap narrows compared to younger demographics. For an 80-year-old, a tobacco user can expect to pay roughly 30% to 45% more per month than a non-tobacco user of the same age and gender. While sub-optimal, this is vastly different from age 40, where smoking can easily triple or quadruple base monthly premium costs.

Can cognitive decline or an early dementia diagnosis disqualify an 80-year-old from simplified issue coverage?

Yes. In 2026, underwriters rely heavily on real-time prescription database queries. If a scan uncovers prescriptions for cognitive medications like donepezil (Aricept) or memantine (Namenda), a simplified issue application will result in an immediate automatic decline. For families navigating cognitive health challenges, a guaranteed issue policy is the only path forward to lock in coverage.

What happens if my parent has a policy but we can no longer afford the monthly premium?

Because final expense and permanent GUL policies build up small amounts of cash value over time, you have consumer protections available before the policy simply lapses. You can contact the carrier to execute a “reduced paid-up” option. This stops all future monthly premium payments entirely, freezing the policy in place with a smaller, adjusted death benefit that remains permanently active until passing.

Conclusion: Securing Peace of Mind at 80 and Beyond

Answering the core question of can an 80 year old get life insurance reveals that the insurance market remains highly accommodating to octogenarians, provided you align your goals with realistic expectations. At this stage of life, attempting to secure a massive corporate-style income replacement framework is a recipe for frustration and financial strain. Instead, focusing your strategy on permanent, right-sized final expense protection ensures your family is entirely insulated from sudden, out-of-pocket burial bills or lingering medical costs.

Remember Aunt Martha? By bypassing the heavily marketed television offers that mandated a strict two-year waiting window, we were able to find a localized simplified issue whole life policy that accepted her controlled high blood pressure. It gave her immediate, day-one coverage for a predictable $10,000 benefit at a price that comfortably fit her fixed retirement budget.

Do not let the fear of advanced age keep you from exploring options. Gather your prescription history, prioritize simplified questionnaires that feature health questions to skip the waiting period, and use independent tools to review your choices. Ultimately, when you ask can an 80 year old get life insurance?, the answer is a definitive yes, as long as you shop smart and pick the right underwriting path for your specific health needs.